What Does It Really Cost to Buy a Home in DC or Maryland in 2026?

The purchase price of a home in DC or Maryland is only the beginning of the conversation. The real cost of homeownership — what you actually spend every month and every year — is substantially higher than the mortgage payment alone, and the gap between 'what the lender approved you for' and 'what you can comfortably afford' is where buyers get into trouble. In this market, a $500,000 home in Washington DC and a $500,000 home in Montgomery County will have meaningfully different true monthly costs — different property taxes, different insurance averages, and different maintenance profiles — even at the same purchase price.

This article gives you the complete picture: every cost layer, real dollar amounts for each, and side-by-side comparisons across all three markets we serve — Washington DC, Montgomery County, and Prince George's County. By the end, you'll be able to build a realistic true monthly cost estimate for any home you're considering.

Layer 1: The Mortgage Payment — Your Biggest Number

The mortgage payment is the foundation, but it's not the whole structure. Let's nail it down precisely so everything else builds on an accurate base.

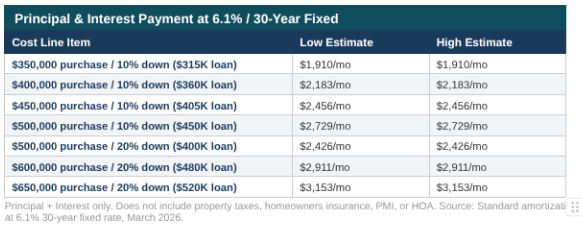

At the current 30-year fixed rate of approximately 6.1% (Freddie Mac, mid-March 2026), here's what principal and interest alone look like at different purchase prices and down payment scenarios:

Two important additions to the raw P&I number:

Private Mortgage Insurance (PMI): If your down payment is less than 20%, expect to add $100–$250/month in PMI until you reach 20% equity. On a $450,000 loan, PMI typically runs $112–$225/month depending on your credit score and loan type.

Jumbo loan territory: In DC and the Maryland suburbs, conforming loan limits for 2026 are $806,500 for single-family homes in high-cost counties. Loans above this threshold are jumbo loans and may carry rates 0.25–0.5% higher, which meaningfully affects the payment calculation.

The lender's pre-approval amount is a ceiling, not a target. Most lenders will approve you for 43–45% debt-to-income, but a payment at that ceiling leaves very little cushion for the other cost layers in this article. Many experienced buyers target a payment at 28–32% DTI to keep breathing room.

Layer 2: Property Taxes — Where DC and Maryland Are Very Different

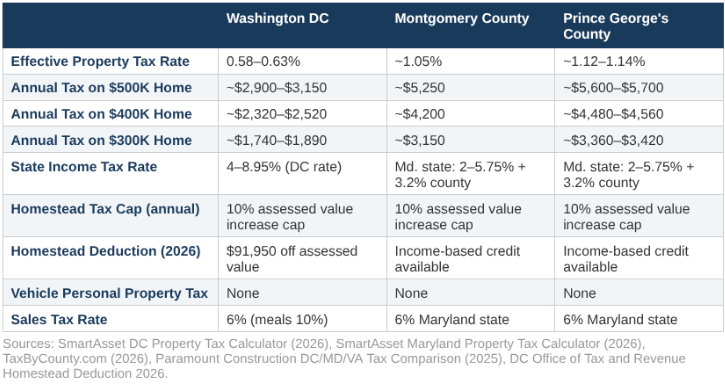

This is the cost layer that most surprises buyers comparing DC and Maryland, and it cuts in a direction most people don't expect: Washington DC has one of the lowest effective property tax rates in the entire country, while the Maryland suburbs — particularly Prince George's County — have rates nearly twice as high.

Let me translate the rate differences into annual and monthly dollar amounts that actually matter for your budget:

A $600,000 home in DC: approximately $3,480–$3,780 per year in property taxes ($290–$315/month). The DC Homestead Deduction of $91,950 (2026) reduces your assessed value meaningfully if this is your primary residence — the effective rate is often closer to 0.58–0.63% after deductions.

A $600,000 home in Montgomery County: approximately $6,300 per year ($525/month). Montgomery County's effective rate of ~1.05% includes the state rate, county rate, transit tax, and MNCPPC assessment.

A $500,000 home in Prince George's County: approximately $5,600–$5,700 per year ($467–$475/month). PG County's effective rate of ~1.12–1.14% is the highest of the three markets.

The practical implication: two buyers purchasing $500,000 homes — one in DC and one in PG County — will have a property tax difference of approximately $2,500–$2,800 per year, or roughly $210–$235 per month. That's a real number. It's also one reason why DC's seemingly higher purchase prices are somewhat offset by its unusually low property tax rate.

Maryland's Homestead Tax Credit caps annual increases in assessed property value at 10% for primary residences — which provides meaningful protection against rapid assessment increases after you buy. But it only applies to your primary residence, and it takes a full tax cycle to kick in after purchase. Budget for the full assessed-value tax in year one.

Layer 3: Homeowners Insurance

Homeowners insurance in Maryland averages $1,537 per year — approximately $128 per month — for a $300,000 dwelling, per SECU Credit Union's Maryland homeownership data. For higher-value homes, the premium scales roughly proportionally, though large homes often have more competitive per-dollar rates with the right carrier.

Real factors that affect your premium in this market:

Home age and construction type: Older homes — particularly in DC's rowhouse stock and inner-ring Maryland neighborhoods — often carry higher premiums due to older electrical systems (knob-and-tube or aluminum wiring), aging plumbing (galvanized steel, cast iron), and proximity to other structures. If you're buying a pre-1970 home, budget toward the higher end of the range.

Flood zone status: Several areas in Montgomery County (along Rock Creek and the Potomac) and Prince George's County have FEMA flood designations. If your property is in a Special Flood Hazard Area, your lender will require a separate flood insurance policy — typically $1,000–$2,500 per year additional. Always check the FEMA flood map for any property you're seriously considering.

Umbrella / liability: Many buyers in this market add umbrella liability coverage at $150–$300 per year once they become homeowners. Not required, but worth including in your full cost picture.

Practical estimates by home value:

$350,000–$400,000 home: approximately $1,400–$1,700/year ($117–$142/month)

$450,000–$550,000 home: approximately $1,700–$2,200/year ($142–$183/month)

$600,000–$700,000 home: approximately $2,200–$2,800/year ($183–$233/month)

Layer 4: HOA Fees — Present in 40% of DC and Maryland Homes

Approximately 40% of homes for sale in this market have a homeowners association, per industry data, with median HOA costs around $125 per month overall — but that average is heavily pulled down by low-fee townhouse communities. The real range is:

Condos in DC and the Maryland suburbs: HOA fees of $300–$800/month are typical, and in some luxury buildings they run $1,000–$2,000+. Critically, condo HOA fees often include water, trash, exterior maintenance, master insurance policy on the building structure, and sometimes gas or heat — so the headline fee isn't always a pure addition to costs.

Townhouses and planned communities: HOA fees typically run $100–$350/month and cover common area maintenance, snow removal in some communities, and amenity access (pool, clubhouse, gym).

Single-family detached homes: Many have no HOA at all. Where HOAs exist, fees typically range from $50–$200/month for basic services.

One cost that buyers frequently underestimate: HOA special assessments. These are one-time charges levied when a community needs a major repair — a new roof on a condo building, parking lot resurfacing, elevator replacement — that exceeds what's in the reserve fund. In older DC condo buildings especially, special assessments of $5,000–$15,000 per unit are not unusual. Before making an offer on any condo, request the HOA's financials, reserve fund study, and meeting minutes to assess the likelihood of special assessments.

When evaluating a condo with a high HOA fee, always calculate the 'all-in' monthly cost: mortgage P&I + property taxes + condo fee. Then compare that to a comparable single-family home's PITI + maintenance reserve. The all-in comparison often makes the condo more — not less — expensive than it first appears.

Layer 5: Maintenance and Repairs — The Cost Layer Most Buyers Ignore

This is the cost layer that separates experienced homeowners from first-time buyers who feel blindsided a year after closing. Every home requires ongoing maintenance — and in a market with a significant stock of older homes, that maintenance bill can be substantial.

The industry standard guidance is to budget 1% of your home's value per year for maintenance and repairs. A $450,000 home = $4,500/year ($375/month) in maintenance reserve. For older homes — pre-1980s construction, which describes much of DC and the inner-ring Maryland suburbs — 1.5% is more realistic: that's $6,750/year on a $450,000 home.

What does that maintenance budget actually cover? It's not one big annual expense — it's the accumulation of smaller regular costs plus occasional larger ones:

HVAC servicing: $150–$300/year for a service contract; replacement when systems fail costs $5,000–$12,000 for a full system

Roof maintenance and eventual replacement: $500–$2,000 for repairs; $10,000–$20,000+ for a full replacement depending on size

Exterior painting: $3,000–$8,000 every 7–10 years for a typical DC rowhouse or Maryland single-family

Water heater: $1,000–$1,800 replacement every 10–15 years

Appliance replacements: $500–$2,500 per appliance; expect to replace most appliances within a 10-year window

Plumbing and electrical: Variable, but older DC and Maryland homes frequently have deferred maintenance in these systems that surfaces in the first few years of ownership

One DC-specific issue worth calling out directly: many rowhouses and older MD homes have shared party walls, aging sewer lines, and foundation situations that are simply different from newer suburban construction. A sewer scope inspection ($150–$300) before purchase is one of the best investments a buyer in this market can make — sewer line replacement in DC can run $8,000–$25,000 and is not covered by homeowners insurance.

The maintenance budget isn't an expense you'll necessarily spend every year. Think of it as a reserve you're building: a $375/month maintenance contribution means $4,500 in year one, $9,000 after two years. When the furnace fails in January, you're drawing from a reserve you built — not scrambling for a credit card.

Layer 6: Utilities — Significantly Higher Than an Apartment

Buyers moving from an apartment — where utilities are sometimes included or split — often underestimate the utility costs of a standalone home. In DC and Maryland's climate (four full seasons, hot humid summers, cold winters), utility costs are a real line item.

Current estimates for the DC and Maryland area:

Electric: $120–$160/month average for a single-family home. Older homes with poor insulation, original windows, or inefficient HVAC systems can reach $200–$250/month in peak summer and winter months.

Natural gas (for heating or cooking): $60–$100/month on average; higher in winter for gas-heated homes. DC-area shelter costs were up 3.5% year-over-year per the Bureau of Labor Statistics November 2025 regional CPI — utility costs have been rising in step with this trend.

Water and sewer: Included in some HOA fees; approximately $60–$100/month where billed separately.

Internet: $50–$120/month depending on provider and speed tier. Most DC and Maryland neighborhoods have Comcast/Xfinity and Verizon Fios as competing options — in served areas, Fios is typically faster and more reliable.

Trash collection: Included in property taxes for DC residents. In Maryland counties, typically included in county services; some municipalities bill separately at $20–$40/month.

Total utility budget for a single-family home in DC or Maryland: $350–$550/month. For a condo where some utilities are included in the HOA fee, the out-of-pocket utility bill is typically $150–$250/month for electric and internet alone.

What It Really Costs Per Month: Three Real Buyer Scenarios

Let's put all six layers together for three representative buyer profiles in this market. These are real numbers — not the mortgage payment the listing ad implies, and not the lender's approval letter. This is the full monthly cost of owning each home.

Three things stand out from these scenarios:

DC's dramatically lower property tax rate (0.63% effective vs. 1.05–1.12% in Maryland) partially offsets its higher purchase prices. At a $650,000 purchase price, a DC buyer pays approximately $340/month in property taxes vs. $570–$610/month for an equivalent home in the Maryland suburbs.

HOA fees are the most variable line item and the one that most dramatically changes the true monthly cost. A condo with a $500/month HOA fee at the same purchase price as a single-family home with no HOA is a fundamentally different cost structure — and the HOA fee compounds over time with increases.

The maintenance reserve is the cost layer most buyers skip in their budgeting — and the one most likely to create financial stress in years two through five of ownership. Budget for it from day one.

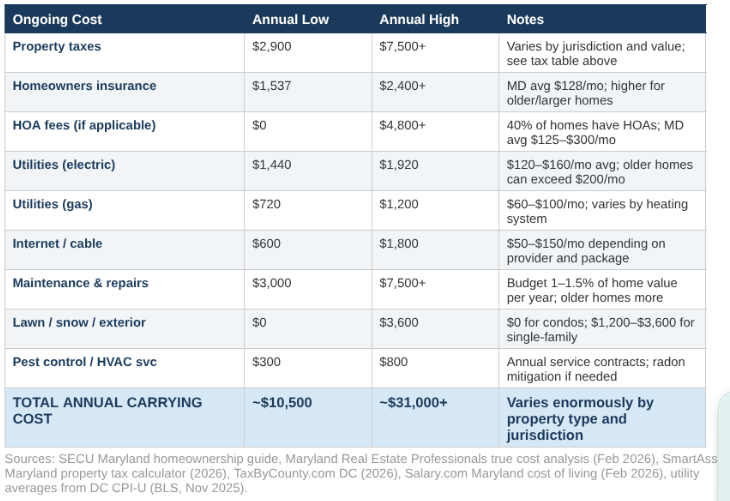

The Full Annual Carrying Cost: All the Non-Mortgage Costs in One Place

Here's a summary of every ongoing cost beyond the mortgage, across realistic low-to-high ranges for DC and Maryland homeowners:

The range between the low and high estimates — $10,500 to $31,000+ per year — is so wide because it depends on: property type (condo vs. single-family), HOA presence, home age and condition, jurisdiction, and lifestyle choices like lawn care. What matters is that you build your specific estimate before you make an offer, not after.

The Upfront Costs: What You Need at Closing

Beyond the ongoing monthly costs, buying a home in DC or Maryland requires significant liquid capital at closing. Here's the complete upfront cost picture:

Down payment: 3–20% of purchase price. On a $500,000 home: $15,000 (3%), $25,000 (5%), $50,000 (10%), or $100,000 (20%).

Closing costs: 2–5% of purchase price in Maryland; 3–5% in DC. On a $500,000 purchase, budget $10,000–$25,000 in closing costs — including lender fees, title charges, and the transfer/recordation taxes detailed in Post 4 of this series. Maryland closing costs average $14,721 per SECU data.

Earnest money deposit: 1–3% of purchase price, wired within 1–3 days of accepted offer. Applied to your down payment and closing costs at settlement, but must be liquid immediately when you go under contract.

Inspection fees: $400–$800 for a standard home inspection, plus $100–$200 for radon, $75–$125 for termite/WDO, and $150–$300 for a sewer scope if recommended. Budget $750–$1,400 total for inspections.

Initial reserves: Most lenders require 2–3 months of PITI payments in the bank after closing. This is on top of your down payment and closing costs — not the same funds.

Total liquid capital needed at closing on a $500,000 home with 10% down in Maryland: approximately $70,000–$80,000 (down payment $50,000 + closing costs $15,000–$20,000 + reserves $8,000–$12,000 + inspections $1,000–$1,400). This is the number that often surprises buyers who focused only on the down payment figure.

The $70,000–$80,000 total cash requirement on a $500,000 Maryland purchase is the number I walk every out-of-state client through in our first conversation. If that number isn't available, the right response isn't to borrow it or stretch into a higher down payment loan — it's to look at lower price points, explore first-time buyer assistance programs, or build savings for 6–12 more months before buying.

Frequently Asked Questions

Q: What is the average monthly cost of owning a home in Montgomery County, Maryland in 2026?

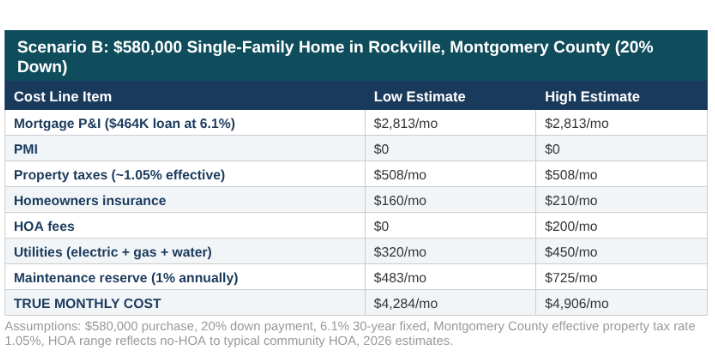

For a typical $580,000 single-family home in Montgomery County with 20% down at today's rates, total true monthly costs run approximately $4,300–$4,900 per month — including mortgage P&I (~$2,813), property taxes (~$508), homeowners insurance (~$160–$210), HOA fees (varies by community, $0–$200+), utilities (~$320–$450), and a maintenance reserve (~$483–$725). The most variable line items are HOA fees and maintenance — an older home without an HOA can run close to $4,300/month; a newer community with a full HOA and higher maintenance needs can push toward $5,000.

Q: Why are property taxes lower in DC than in the Maryland suburbs?

Washington DC has an effective residential property tax rate of approximately 0.58–0.63% — one of the lowest in the country — compared to ~1.05% in Montgomery County and ~1.12% in Prince George's County. DC's low rate exists alongside high property values, which means the dollar tax bill is still substantial on an expensive home. But it does mean that two homes at the same price — one in DC, one in Maryland — will have meaningfully different property tax bills. On a $600,000 home, the DC annual tax is roughly $3,500–$3,800 vs. $6,300–$6,800 in the Maryland suburbs.

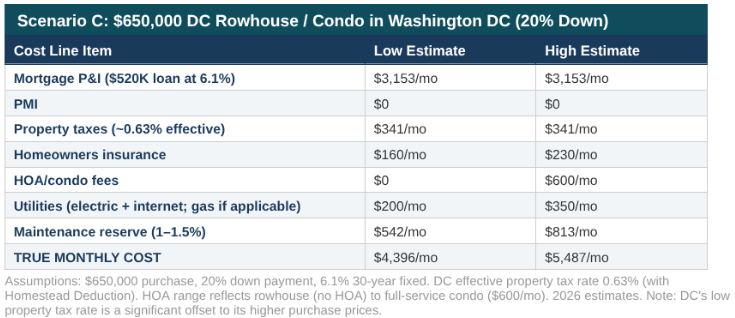

Q: What is the true monthly cost of owning a condo in Washington DC?

For a $650,000 DC condo with 20% down, the true monthly cost runs approximately $4,400–$5,500 depending heavily on HOA fees. The mortgage P&I is approximately $3,153/month. DC's low property taxes add about $341/month. Homeowners insurance is modest ($160–$230/month). But condo HOA fees range from $200 to $600+/month in DC's building stock, and that range is the primary driver of variation. Higher HOA fees in full-service buildings often include amenities and building maintenance that offset some costs, but they also tend to rise annually. Always calculate the full all-in monthly cost before comparing condo options.

Q: How much should I budget for home maintenance in DC or Maryland?

Budget 1% of your home's purchase price per year as a maintenance reserve — $4,000/year on a $400,000 home, $5,000/year on a $500,000 home. For older homes (pre-1980), budget 1.5% — older DC rowhouses and inner-ring Maryland homes have aging systems that tend to require more frequent attention. This reserve covers routine maintenance plus builds a cushion for larger unexpected repairs. The 1% rule is an average — some years you'll spend more, some years less — but the reserve should be funded consistently from month one of ownership.

Q: Is it cheaper to own a condo or a single-family home in the DC area?

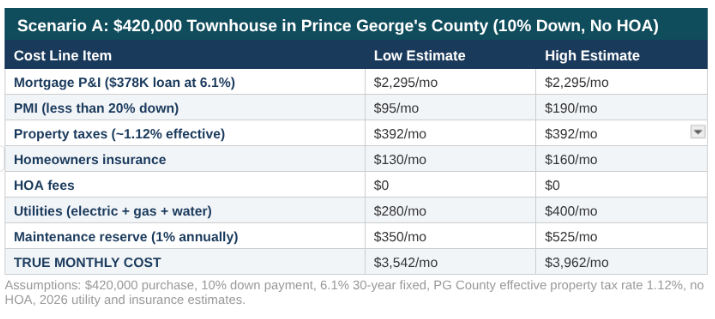

On a true monthly cost basis, it depends heavily on the specific HOA fee and the home's age and condition. A single-family home with no HOA in Prince George's County at $420,000 might run $3,500–$4,000/month all-in. A DC condo at the same purchase price with a $400/month HOA fee could run $4,000–$4,400/month. The condo's lower maintenance responsibility (the HOA handles exterior and common area) partially offsets its HOA cost. The most important comparison is always the full all-in number, not the purchase price or the mortgage payment in isolation.

Q: Does Maryland have higher closing costs than other states?

Yes. Maryland has some of the highest buyer closing costs on the East Coast, averaging approximately $14,721 or about 3.7% of median home price, according to SECU Credit Union data. The primary driver is Maryland's transfer and recordation tax structure, which is among the highest in the country. In Montgomery County specifically, the recordation tax rate is tiered and can reach 2.27% on higher purchase amounts. DC's closing costs are similarly high, with transfer taxes at 1.1–1.45% of the purchase price. First-time buyers in both jurisdictions receive meaningful tax exemptions that can reduce closing costs by $2,000–$4,000 — confirm your eligibility with your lender and title company early.

The Right Way to Think About Affordability in This Market

The number a lender approves you for is the ceiling, not the floor. Real affordability in this market — the kind where you can absorb a furnace replacement without financial panic, where you're building reserves rather than depleting them, where the monthly payment doesn't feel like a tightrope — means buying below your maximum approval and budgeting for every layer in this article.

I build a complete true-cost analysis for every buyer I work with before we make an offer. Not because I want to talk anyone out of buying — I want to help you buy confidently, not reluctantly. But 'confidently' means knowing the real number before you commit to it, not after.

If you're trying to figure out what a specific property or price range actually costs per month in this market — all in — that's a 20-minute conversation I'm happy to have with you.

Want to Know What Your Specific Home Will Cost Per Month — All In?

Let’s run a specific cost analysis for the properties you’re interested in together — mortgage, taxes, insurance, HOA, and maintenance reserve — before we make an offer, not after. No surprises at closing, and no surprises six months later.

Call or text me and let's run your numbers.

Email: Ryan.Hehman@compass.com | Direct: 443-990-1230

Free consultation. No obligation. Real numbers.

Related articles on this site:

Relocating to Washington DC & Maryland: The Complete 2026 Guide from a Local Expert

Is It Better to Rent First or Buy Immediately When Moving to the DC Area?

DC vs. Maryland Suburbs: Where Should You Actually Live When Relocating to the DC Area?

How to Buy a Home in DC or Maryland Before You Move: A Step-by-Step Guide for Out-of-State Buyers

Is 2026 a Good Time to Buy a Home in DC or Maryland? What the Data Actually Says