How to Buy a Home in DC or Maryland Before You Move: A Step-by-Step Guide for Out-of-State Buyers

If you're moving to Washington DC or the Maryland suburbs from out of state and trying to figure out how to buy a home before you arrive, here's the most important thing to know: it's entirely doable, and buyers who are well-prepared and working with the right local agent close on homes every month in this market without ever setting foot in a neighborhood until moving week. But the sequence matters enormously. Out-of-state buyers who skip steps — who start browsing Zillow before they have financing in order, or who tour homes virtually without first narrowing the geography — waste months of effort and regularly lose out to buyers who did the work in the right order.

This guide is the step-by-step process I walk every out-of-state relocation client through. It's built around the realities of the DC and Maryland market specifically — the jurisdictional complexity, the closing cost structure, the inspection requirements, and the competitive dynamics that make this market different from most of the country. Follow it in order, and you'll be in a strong position to buy confidently, even from a thousand miles away.

I'm Ryan Hehman, a real estate agent serving Washington DC and the Maryland suburbs — primarily Montgomery County and Prince George's County. I work with relocation buyers regularly, and I've built a process specifically for people who need to buy in a market they don't yet know. Here's exactly how we do it.

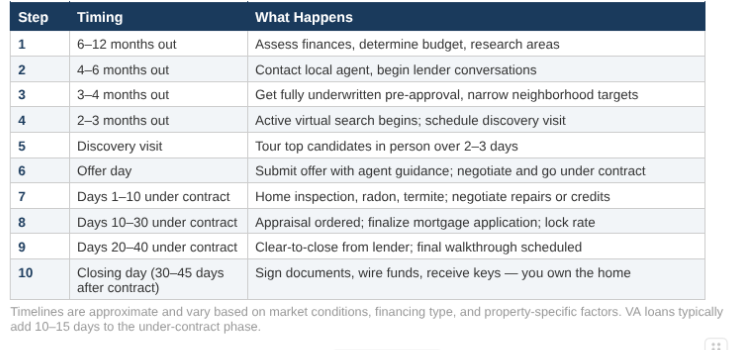

The Full Timeline at a Glance

Before the step-by-step detail, here's the complete process in one place — so you can see how the pieces fit together and map it to your move date.

Assess Your Finances and Set a Realistic Budget ⏱ 6–12 months before your move

Most out-of-state buyers underestimate their budget — in both directions. They either overestimate what they can afford based on their home market, or they assume DC and Maryland are unaffordable and don't look seriously. The right starting point is the actual numbers, not assumptions.

The three figures you need to know before anything else:

Your gross monthly income — this is what lenders use to calculate how much mortgage you can carry. The standard guideline is that your total monthly housing costs (principal, interest, taxes, and insurance — PITI) should not exceed 28% of gross monthly income. Your total debt payments including the mortgage should not exceed 43–45%.

Your available down payment and closing cost reserves. In Maryland, closing costs for buyers typically run 2–5% of the purchase price on top of your down payment — and this market has some of the highest transfer and recordation taxes in the country. Budget for both. A $500,000 purchase with 10% down ($50,000) plus 3% closing costs ($15,000) requires $65,000 in liquid funds at closing.

Your credit score. Conventional loans typically require a minimum 620–640 credit score; the best rates go to buyers at 740 and above. FHA loans allow scores as low as 580 with 3.5% down. VA loans have no minimum score requirement, though most VA lenders want 620+. Pull your credit report before you start the process so there are no surprises.

One thing I tell every relocation client explicitly: the DC and Maryland market has enough price range that almost every budget has a viable path. A household income of $90,000 can buy in Prince George's County. A household income of $200,000+ opens up much of Montgomery County and DC proper. The key is knowing which market matches your number before you start investing emotional energy in listings.

Rule of thumb: multiply your gross annual household income by 4.5 to get a rough maximum purchase price at current rates. A $120,000 household income = approximately $540,000 maximum. That's a starting point — a lender conversation will give you the precise figure.

2. Find a Local Agent Who Specializes in Relocation Buyers

⏱ 4–6 months before your move

This step comes before the lender conversation — or at the same time — because the right local agent will help you navigate both. Here's why finding the right agent matters more in this market than most:

DC, Montgomery County, and Prince George's County are three different jurisdictions with different contract forms, different tax structures, different inspection customs, and different competitive dynamics. An agent who primarily works one area may give you incomplete or inaccurate guidance for another. You want someone who works across the markets you're considering and understands the differences at a granular level.

For out-of-state buyers specifically, your agent is your eyes, ears, and local intelligence. They'll tell you which blocks in a given neighborhood feel different from the listing photos, which streets have commute issues that Google Maps won't show you, which sellers are genuinely motivated versus just testing the market, and which inspection items are normal for the area versus genuine red flags. That kind of hyperlocal knowledge is not replaceable by research from a distance.

What to look for when evaluating agents for a relocation purchase:

Experience specifically with out-of-state and relocation buyers — this requires a different process than local buyers and not every agent has developed it

Familiarity with all three jurisdictions you're considering (DC, Montgomery County, PG County), not just one

Willingness to do video walkthroughs with commentary, not just forward you Matterport links

A clear process for remote buyers — they should be able to tell you exactly how they handle offers, inspections, and closing for buyers who aren't local

References from relocation buyers specifically — ask for them

The agent relationship for a relocation buy is closer to a guide relationship than a transaction relationship. You're trusting this person's judgment on a market you don't know yet. Take the vetting seriously.

3. Get a Fully Underwritten Pre-Approval — Not Just a Pre-Qualification

⏱ 3–4 months before your move

There are two different things lenders offer, and the difference matters significantly in this market. A pre-qualification is a quick estimate based on self-reported information — income, assets, debts — with no document verification. A fully underwritten pre-approval means a lender has verified your income documents, run your credit, reviewed your assets, and issued a conditional commitment to lend. In a competitive DC or Maryland market, sellers and listing agents know the difference.

Why this matters specifically for out-of-state buyers: when you make an offer on a home you've seen virtually, you're already asking the seller to accept more uncertainty than they face from a local buyer who toured in person. A fully underwritten pre-approval removes one of the biggest uncertainties and signals that your offer is financeable — not just interested.

What you'll need to gather for a full pre-approval:

Two years of W-2s or 1099s (plus tax returns if self-employed or with complex income)

Two most recent pay stubs

Two to three months of bank statements for all accounts you'll use for the down payment and closing costs

Government-issued ID

Authorization to run your credit

One important note on lender selection: use a local lender or one with specific experience in the DC and Maryland market. Maryland's transfer and recordation tax structure, its specific title company customs, and the jurisdiction-specific contract timelines can trip up out-of-state lenders who don't know the market. A lender who does deals in this area regularly will get you fewer surprises on your Loan Estimate and smoother communication through the transaction.

Pre-approvals are typically valid for 60–90 days. If your timeline extends beyond that, you'll need a refresh — not a full new application, but an updated credit pull and document review. Plan for this if your move is more than three months out.

4. Narrow Your Geography Before You Start Browsing Listings

⏱ 3–4 months before your move

This is the step most out-of-state buyers skip, and it's the one that wastes the most time when skipped. The DC and Maryland area has enough jurisdictional complexity and neighborhood variation that browsing listings without a geographic focus is like searching a store without knowing what you need. You end up looking at hundreds of properties in four different counties, none of which you know well enough to evaluate seriously.

The geography-narrowing conversation with your agent should answer three questions:

What is your workplace address, and which Metro line — or which driving corridor — connects you to it? Your commute anchor should drive your neighborhood targeting more than any other single factor.

What is your honest price range based on your pre-approval, and which jurisdictions have meaningful inventory in that range? (See Post 1 in this series for the full DC vs. Montgomery County vs. Prince George's County comparison.)

What are your two or three non-negotiables — schools, walkability, yard size, specific neighborhood feel — that will eliminate markets from consideration?

The output of this conversation should be a short list of two to four target neighborhoods or areas, not a county-wide search. This is what makes virtual searching productive: instead of browsing 200 listings across a 30-mile radius, you're watching a specific Zillow saved search for Silver Spring and Takoma Park, and your agent is alerting you when something new hits the market in those areas.

The DC area's neighborhood-level variation also means that being half a mile in the wrong direction can mean a different school district, a meaningfully longer commute, or a different property tax bill. Your agent should walk you through a specific boundary map of your target areas — not just a general market overview.

5. Run Your Virtual Search Strategically ⏱ 2–3 months before your move

Once you've narrowed your geography and your pre-approval is in hand, you're ready to search actively. For out-of-state buyers in 2026, the virtual search toolkit is genuinely strong — better than it's ever been. Here's how to use it effectively:

3D Virtual Tours and Matterport

Most well-listed properties in the DC and Maryland market now include Matterport 3D tours or equivalent virtual walkthroughs. These let you navigate through the home room by room, see spatial relationships, check ceiling heights, and get a much more accurate sense of the property than photos alone. High-end 3D tours also include measurement tools — you can measure whether your furniture will fit before you make an offer. Always request a Matterport or equivalent before putting a property on your serious consideration list.

Agent Video Walkthroughs

This is the tool that separates remote buyers who make good decisions from those who get surprised. Ask your agent to walk through any serious candidate on video — live via FaceTime or Zoom, or recorded with commentary. A good agent walkthrough covers what the photos don't show: the slope of the yard, the noise from the nearby road, the condition of the mechanicals in the basement, the feel of the street at the end of the driveway. This is qualitative information that no listing platform captures, and it's your most important research tool as a remote buyer.

What a Matterport tour won't tell you: what the basement smells like, whether the neighbor's house is impeccably maintained or neglected, how loud the nearby intersection is during rush hour, or whether the 'updated kitchen' was done by a professional or a DIY enthusiast. Your agent's walkthrough fills that gap.

Neighborhood Research from a Distance

Google Street View is more useful than most buyers realize — use it to walk the street virtually, see the scale of the lot, check the condition of adjacent properties, and get a visual sense of the block. Google Maps satellite view shows proximity to parks, infrastructure, and neighboring uses. Local Facebook neighborhood groups, Reddit's r/washingtondc, and Nextdoor are all worth 30 minutes of reading to understand the local community voice in any neighborhood you're seriously targeting.

What remote research can't fully replace: visiting at different times of day, feeling the commute from that address, and walking the neighborhood at street level. Plan to do at least one in-person visit before committing to an offer if at all possible. But the virtual groundwork you do beforehand makes that visit dramatically more efficient.

6. Plan Your Discovery Visit — Make It Count

⏱ Schedule 6–8 weeks before target purchase

A discovery visit — typically a long weekend in the market — is the single highest-ROI activity in a relocation purchase. Two and a half days on the ground, done well, will tell you more about your target neighborhoods than months of remote research. Here's how to make the most of it:

Plan it with your agent in advance, not spontaneously. Share your shortlist of properties and target neighborhoods before you arrive, so your agent can schedule tours efficiently and build an itinerary that covers both the homes and the surrounding area.

Tour more than the properties — tour the neighborhoods. Ask your agent to drive you from your target home to your workplace during morning rush hour, so the commute isn't a theoretical Google Maps estimate. Walk to a nearby coffee shop or grocery store. Sit in a park for a few minutes. Arrive with the question 'could I live here?' and answer it from the street, not from a listing page.

See your top two or three candidates in person, not ten. Overloading a single visit with too many properties creates decision fatigue and makes every home start to blur together. Use your virtual pre-work to pre-qualify down to a short list, then give each serious candidate real attention on the visit.

Budget for a second visit if needed. If your first visit clarifies the geography but doesn't produce an offer-ready candidate, a second focused visit — often just one or two homes — is a reasonable investment in getting the decision right.

Take notes and photos your agent doesn't take. Listing photos and even agent walkthrough videos are optimized for the property's best features. Your personal notes and candid photos during the visit capture the things that matter to your daily life — the ceiling height in the living room where your sectional goes, the bathroom counter space, the garage door clearance for your car.

The buyers who get the most out of a discovery visit are the ones who arrive with a clear set of non-negotiables already defined and use the visit to confirm or disqualify, not to explore from scratch. Do the exploration remotely. Use the visit to decide.

7. Make a Competitive Offer — With Remote Buyer Strategy

⏱ When the right property appears

When you find the right property — whether during a visit or identified remotely — the offer process as an out-of-state buyer requires a few specific strategic considerations beyond what a local buyer faces.

Offer Terms That Compensate for Remote Buyer Perception

In a competitive situation, sellers sometimes view out-of-state buyers as slightly higher risk than local buyers — not because of financing, but because of the assumption that remote buyers may not have fully seen the property and might back out. You can counter this perception with offer terms that signal commitment:

Include your fully underwritten pre-approval letter, not just a pre-qual — this alone addresses most seller concerns about financing reliability

Offer a strong earnest money deposit — in the DC area, earnest money is typically 1–3% of the purchase price. Coming in at the higher end signals seriousness

If you've done a video walkthrough with your agent and feel confident about the property's condition, consider waiving or shortening the home inspection contingency period.

A cover letter briefly noting that you've done extensive virtual research including a live video walkthrough with your agent can help humanize a remote offer

Escalation Clauses

If you're in a multiple-offer situation on a property you've researched thoroughly and feel confident about, an escalation clause — where your offer automatically increases by a set increment above any competing offer, up to a maximum price — is a useful tool for out-of-state buyers who can't as easily come back for a second showing or counter-offer round. Your agent can advise on when escalation clauses are appropriate for specific properties.

Earnest Money Deposit Logistics

Once your offer is accepted, you'll typically need to wire your earnest money deposit (1–3% of purchase price) to a title company within 1–3 business days. As an out-of-state buyer, set up your wire transfer process in advance — know which bank account you're wiring from and confirm the wire instructions directly with the title company by phone before sending any funds. Wire fraud in real estate transactions is a real risk, and the DC area has not been immune to it. Always verify wire instructions verbally, never from an email alone.

8. Navigate Inspections Remotely — What DC and Maryland Require

⏱ Days 1–10 under contract

Home inspections in DC and Maryland have a few specifics that out-of-state buyers need to understand — and they're different from what you may have experienced in other markets.

The Standard Home Inspection

A standard home inspection in the DC and Maryland area costs approximately $300–$600 and covers the structure, systems (HVAC, plumbing, electrical), roof, foundation, and general condition. As a remote buyer, you have two options: (1) attend the inspection via video with your inspector sharing their screen or a live feed, which most inspectors in this market are comfortable accommodating, or (2) have your agent attend on your behalf and call you with any significant findings during the inspection. I strongly recommend attending virtually — your inspector's live commentary will tell you far more than a written report after the fact.

Maryland-Specific Inspections

Maryland has specific inspection requirements that differ from other states:

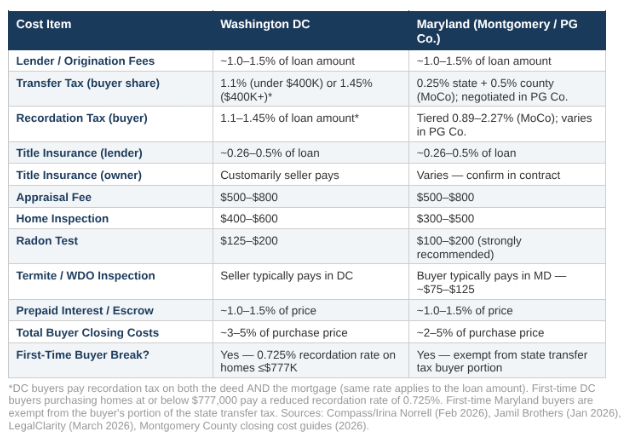

Radon testing is strongly recommended — Maryland has areas with elevated radon levels, and it's a $100–$200 addition to your inspection that frequently reveals issues. If radon is present above the EPA action level (4 pCi/L), remediation is typically a $1,500–$2,500 repair and is routinely negotiated as a seller credit.

Termite / Wood Destroying Organism (WDO) inspection: In Maryland, the buyer customarily pays for this — approximately $75–$125. In DC, the seller typically pays. Confirm this in your contract.

Sewer scope inspection: Not standard in every transaction, but strongly recommended for older homes (pre-1980s), particularly in DC and inner-ring Maryland neighborhoods where clay or cast iron sewer lines are common. A sewer scope typically costs $150–$300 and can reveal $5,000–$20,000+ in deferred maintenance.

Negotiating After Inspection

After your inspection, you have several options in the DC and Maryland contract framework: request repairs, request a credit at closing (often more efficient than demanding specific repairs), accept the property as-is, or in cases of significant undisclosed issues, potentially void the contract within the inspection contingency period. Your agent will guide you on what's reasonable to request versus what sellers in this market typically resist. As a remote buyer, having an agent who can advocate clearly on your behalf during this negotiation is one of the highest-value parts of the relationship.

9. Understand the Closing Cost Structure — DC and Maryland Are Different

⏱ Days 10–30 under contract

This is the step where out-of-state buyers most frequently encounter sticker shock, and I want to address it directly so you're not surprised at the closing table. DC and Maryland have some of the highest buyer closing costs in the country, driven primarily by transfer and recordation taxes. Here's the complete picture:

A few things every out-of-state buyer should know about closing costs in this market:

Maryland uses title companies for closing, not real estate attorneys. You'll choose a title company (often with your agent's recommendation) who will conduct the settlement, handle the escrow of your earnest money, and ensure the title transfers cleanly. This is different from states like New York where attorneys conduct closings.

In Maryland, transfer and recordation taxes are presumed to be split 50/50 between buyer and seller under state law — but this is negotiable in your contract. In a buyer-friendly market environment, asking the seller to cover a larger share is worth attempting.

First-time buyers in both DC and Maryland get meaningful tax breaks. In DC, the recordation rate drops from 1.1–1.45% to just 0.725% on homes up to $777,000 — a savings of thousands of dollars. In Maryland, first-time buyers are exempt from the buyer's portion of the state transfer tax. Confirm your first-time buyer status with your agent and title company before closing.

Remote Online Notarization (RON) is now available in Maryland, meaning you can sign your closing documents from your current location via secure video — you don't need to be physically present in Maryland on closing day. Confirm this option with your title company early in the transaction if it applies to your situation.

Budget 2–5% of your purchase price for closing costs in Maryland and DC, on top of your down payment. On a $500,000 purchase, that's $10,000–$25,000 in closing costs alone. The exact amount varies significantly by jurisdiction and whether you qualify for first-time buyer exemptions — get an itemized Loan Estimate from your lender early and review it carefully.

10. Close and Get the Keys — What Happens on Closing Day

⏱ 30–45 days after contract

Closing day in DC and Maryland is typically handled through a title company settlement. Here's what to expect in the final days leading up to it:

Your lender will issue a Clear to Close (CTC) once all underwriting conditions are satisfied — typically 5–7 days before your scheduled closing date. At this point, your rate is locked, your loan is approved, and the finish line is clear.

You'll receive a Closing Disclosure at least three business days before closing that itemizes every cost, credit, and payment in the transaction. Compare it carefully against your original Loan Estimate — the numbers should be close, and any significant changes should prompt a conversation with your lender.

The day before or morning of closing, you (or your agent on your behalf) will do a final walkthrough of the property to confirm it's in the agreed condition — that any negotiated repairs were completed, seller's belongings are removed, and no new issues have appeared.

You'll wire your closing funds — down payment plus closing costs minus your earnest money already in escrow — to the title company. Confirm wire instructions directly by phone before sending. As noted earlier, wire fraud is a real risk in real estate transactions.

On closing day, if you're attending remotely via RON, you'll complete the signing session with the title company via video. If you're attending in person, the signing typically takes 45–75 minutes.

Once all documents are signed and funds are confirmed, the title company records the deed with the county. At that point — in Maryland and DC, typically the same day — you own the home. Your agent will coordinate key handoff.

And with that, you've successfully bought a home in one of the most complex and competitive markets in the country — from out of state. It's entirely doable with the right preparation and the right local team.

Special Situations: VA Loans, First-Time Buyer Programs, and New Construction

VA Loans for Military and Veteran Buyers

If you're a veteran or active military buyer relocating to DC or Maryland, VA loan eligibility is one of your most significant financial advantages and you should use it. VA loans require no down payment, have no private mortgage insurance, and typically offer rates 0.25–0.5% below conventional rates. In the current market, VA loans are absolutely viable — I've helped VA buyers close competitive offers in this market — though the offer strategy requires care in multiple-offer situations, as some sellers have historically favored conventional financing. Your agent should know how to position a VA offer competitively.

Maryland First-Time Buyer Programs

Maryland's Mortgage Program (MMP) is one of the most robust first-time buyer assistance programs in the country. The 1st Time Advantage program offers the lowest 30-year fixed rate available through the state program, often below market rates. The MMP also offers down payment assistance through its flex programs — typically 3–4% of the loan amount as a grant or deferred loan that helps bridge the gap between what a buyer has saved and the full down payment requirement. Income limits and purchase price limits apply; eligibility is worth checking before you assume the programs aren't relevant to you.

Prince George's County offers its own Pathway to Purchase assistance program for first-time buyers purchasing within county limits. Montgomery County has additional programs through the Department of Housing and Community Affairs. These local programs stack on top of state programs in some cases — your lender and agent should both be aware of what's available in the specific county you're buying in.

DC First-Time Buyer Programs

Washington DC has two primary first-time buyer programs worth knowing. DC Open Doors offers below-market first mortgage rates and a deferred zero-interest second loan covering the full minimum down payment — meaning a qualified first-time DC buyer can purchase with essentially no down payment. The Home Purchase Assistance Program (HPAP) provides down payment and closing cost assistance as a deferred, interest-free loan for lower-to-moderate income buyers purchasing in DC. Both programs have income limits, but they extend higher up the income spectrum than many buyers assume — worth checking before you rule them out.

New Construction

New construction is an option worth considering for out-of-state buyers who can handle a longer timeline — typically 6–18 months from contract to delivery. The advantage: you don't need to be local during construction, you get a warranty on systems and structure, and you avoid the inspection uncertainty of an older home. The DC and Maryland area has active new construction in Prince George's County's developing corridors and select Montgomery County submarkets. New construction contracts are heavily weighted toward the builder — having an agent represent you at the purchase table is strongly recommended, and their commission is typically paid by the builder.

Frequently Asked Questions from Out-of-State Buyers

Q: Can I actually make an offer on a home I've never visited in person?

Yes, and it happens regularly in this market. The combination of Matterport 3D tours, live agent video walkthroughs, neighborhood street-view research, and a trusted local agent with eyes on the property means remote buyers can make well-informed offers. The risk isn't zero — you're relying more heavily on your agent's judgment and the virtual research — but it's manageable with the right process. I recommend at least one in-person visit to the area before or shortly after going under contract, even if the offer itself is made remotely.

Q: How do out-of-state buyers handle the home inspection remotely?

Most inspectors in the DC and Maryland market will accommodate remote participation via video call during the inspection — either FaceTime, Zoom, or a similar platform. You observe the inspection in real time, ask questions, and hear the inspector's commentary as they move through the property. This is significantly more valuable than reading the written report afterward. Your agent can also attend in person and serve as a second set of eyes. For out-of-state buyers, I always recommend attending the inspection virtually rather than skipping it.

Q: How long does the closing process take in Maryland and DC?

Closing typically takes 30–45 days from accepted offer to receiving keys, assuming standard conventional financing and no unusual title or inspection complications. VA loans typically add 10–15 days. Cash purchases can close in as little as 14–21 days. Maryland's title company settlement process is well-established and efficient once all parties are moving. The most common delays are financing-related — which is why getting a fully underwritten pre-approval before you begin your search matters so much.

Q: Do I need to be in Maryland or DC on closing day?

No — Maryland allows Remote Online Notarization (RON), meaning you can sign your closing documents via secure video from your current location. Not all title companies offer this, so confirm with your settlement company early in the transaction. DC has different rules; confirm RON availability for DC closings specifically with your agent and title company. For buyers who prefer to attend in person — or whose lender requires physical presence — the signing appointment typically takes 45–75 minutes.

Q: What is earnest money, and how much should I offer in DC and Maryland?

Earnest money is a good-faith deposit made when your offer is accepted, held in escrow by the title company, and applied toward your down payment and closing costs at settlement. It demonstrates to the seller that you're a serious buyer. In DC and Maryland, earnest money is typically 1–3% of the purchase price. In a competitive situation, coming in at 2–3% signals commitment. The earnest money is at risk if you back out of the contract without a valid contingency, so it should reflect your genuine intention to purchase — but it's protected as long as you exercise your inspection, financing, or appraisal contingencies in good faith.

Q: What if the home appraises below my offer price?

An appraisal gap — where the property appraises below your purchase price — is more common when buyers are paying above list price in competitive situations. If this happens, you have three main options: negotiate with the seller to reduce the price to the appraised value (most common), pay the difference between the appraised value and purchase price in cash (requires additional liquid reserves), or void the contract under the appraisal contingency and get your earnest money back (if the appraisal contingency is in place). Including an appraisal contingency in your offer is strongly recommended for most out-of-state buyers, particularly if you haven't toured the property in person.

You Can Do This — With the Right Preparation and the Right Team

Buying a home from out of state in a market as complex and competitive as DC and Maryland sounds daunting from the outside. I want to be honest: it requires more preparation than a local purchase, a stronger reliance on your local agent's judgment, and a willingness to do serious research from a distance. But it is entirely achievable, and I help buyers do it regularly.

The buyers who succeed at this aren't necessarily the ones with the most money or the most flexibility. They're the ones who follow the sequence — get their financing in order first, narrow their geography before they start browsing, work with an agent who takes the remote buyer process seriously, and come to their discovery visit prepared to decide rather than just explore.

If you're at any point in this process — whether you're just starting to assess your budget or you're three weeks from your move date and haven't found a home yet — I'm here to help. The consultation is free, the guidance is honest, and I've been through this process enough times to know where things go right and where they go sideways.

Moving to DC or Maryland from Out of State?

Let's Map Your Plan.

I've helped out-of-state buyers navigate this market from thousands of miles away — from first video call to closing day. In a free 30-minute consultation, I'll help you build a realistic timeline, identify the right neighborhoods for your budget and commute, and understand exactly what to expect from the DC and Maryland buying process before you tour a single home.

Call or text Ryan Hehman | 443-990-1230 | Email: Ryan.Hehman@compass.com

Free relocation consultation. No obligation.

Related articles on this site:

Relocating to Washington DC & Maryland: The Complete 2026 Guide from a Local Expert

DC vs. Maryland Suburbs: Where Should You Actually Live When Relocating to the DC Area?

Is It Better to Rent First or Buy Immediately When Moving to the DC Area?

What Federal Employees and Contractors Need to Know About Buying a Home in DC and Maryland Right Now