Is 2026 a Good Time to Buy a Home in DC or Maryland? What the Data Actually Says

Yes — with one important qualifier. For buyers who are financially prepared, planning to stay in the area for at least five years, and clear on which market they're targeting, 2026 offers the most favorable buying conditions in the DC and Maryland area since 2019. Inventory is up meaningfully across all three markets we serve. Homes are sitting on the market longer, giving buyers more time to evaluate. Sellers are more flexible than they've been in years. And mortgage rates, while not at historic lows, have declined significantly from their 2024 peak and are projected to ease further by year-end.

The qualifier: this market is not uniform. Washington DC proper is showing the most disruption — inventory up over 50% year-over-year and a projected modest price decline — while Montgomery County and Prince George's County are holding steadier with modest appreciation and tighter supply. The right answer for a buyer targeting Bethesda looks different from the answer for a buyer targeting Capitol Hill, which looks different again from a buyer focused on Hyattsville.

This article is my honest read of the data — not a cheerleader pitch and not a fear headline. Let me walk you through what the numbers actually show, market by market, as of March 2026.

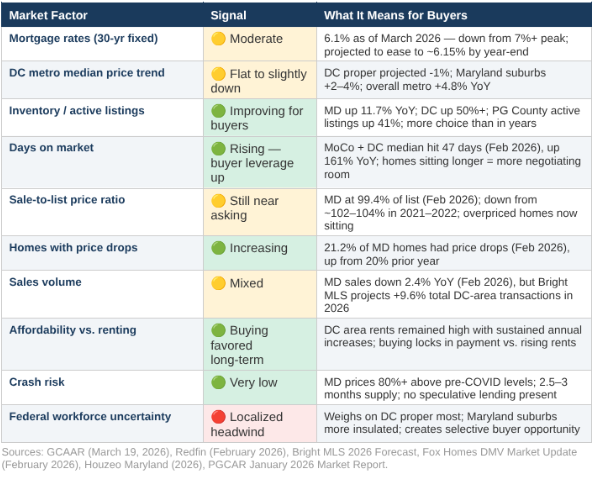

The 2026 DC and Maryland Buyer Scorecard

Before the jurisdiction-by-jurisdiction breakdown, here's a consolidated scorecard of every major market factor and what it means for buyers right now. This is the table I'd hand a client walking into my office for the first time.

Read as a whole, the scorecard tells a consistent story: this is not a buyer's market in the classic sense — inventory is still below the six-month threshold that would tip the scales firmly in buyers' favor. But it is the most balanced market this region has seen since before the pandemic, and buyers who are prepared to move decisively have leverage that simply didn't exist in 2021 or 2022. The question is whether you're in a position to use it.

The Five Forces Shaping the 2026 DC and Maryland Market

Force 1: Mortgage Rates Are Down From Their Peak — and Projected to Ease Further

The 30-year fixed mortgage rate as of mid-March 2026 is approximately 6.1%, per Freddie Mac's weekly survey — down meaningfully from the 7%+ peak in late 2024. Realtor.com projects rates averaging near 6.3% for the full year; Bright MLS projects rates falling to an average of 6.15% by year-end 2026. The Mortgage Bankers Association's forecast is similar, with possible further improvement in the second half of the year if inflation continues to moderate.

Let me translate that into dollar terms. On a $500,000 loan at 7.25% (late 2024 peak), the monthly principal and interest payment is $3,414. At 6.1%, it's $3,042. That's a difference of $372 per month — $4,464 per year — on the same loan amount. That's not nothing. And it's why the Bright MLS forecast projects DC-area home sales transactions to rise 9.6% in 2026 as buyers who were priced out at 7% rates start re-entering the market.

The honest caveat: rates are not going to return to the emergency lows of 2020–2021 (2.65–3.0%). The Freddie Mac historical average since 1971 is approximately 7.8%. From that perspective, 6.1% is below the long-run average, and buyers waiting for dramatically lower rates are likely waiting for a window that won't open. As one mortgage economist put it: when rates go up, they take the elevator. When they come down, they take the stairs.

A 0.5% rate improvement saves a buyer approximately $150/month on a $500,000 loan. But a 2% price increase on that same home adds $10,000 to the purchase price. Chasing a marginally better rate while prices appreciate costs more money than it saves.

Force 2: Inventory Is Rising — Meaningfully, But Not Dramatically

This is the most consequential shift in the market for buyers right now. According to the most current data from GCAAR (released March 19, 2026), there were 3,442 active listings in the Montgomery County and DC area in February 2026 — and housing supply reached 2.6 months, above the five-year average of 1.8 months. That shift represents a significant improvement in buyer options compared to the inventory-constrained environment of 2022–2024.

At the Maryland statewide level, Redfin reports 17,808 homes for sale in February 2026 — up 11.7% year-over-year. Prince George's County PGCAR data shows active listings up 41% in January 2026. Washington DC is seeing the most dramatic shift, with active inventory up over 50% year-over-year, driven in part by federal workforce uncertainty pushing some federal employees to list and others to pause purchases.

Context matters here: even with this inventory increase, the Maryland market sits at approximately 2.5–3 months of supply — still well below the 6 months that defines a balanced market. This is not a buyer's market. It is a significantly less competitive seller's market than the prior three years. The practical implication: you have more options, more time to decide, and more negotiating leverage than at any point since 2019 — but you're not operating in a market where sellers are distressed and discounting freely.

The most actionable inventory insight for buyers: look specifically at homes that have been on the market for 15 days or more without going under contract. In this environment, those listings are where seller motivation and negotiating room are most concentrated.

Force 3: Days on Market Are Rising Sharply — Giving Buyers Time to Think

This is the data point that most clearly signals the market shift in real time. According to GCAAR's February 2026 report (published March 19, 2026), the median days on market in Montgomery County and Washington DC rose to 47 days — a 161% increase compared to the same time last year. That is an extraordinary shift. A year ago, the median home in this market was under contract in under 20 days. Today it's sitting for seven weeks on average.

At the Maryland statewide level, Redfin reports median days on market of 56 days in February 2026, up 13 days year-over-year. In the same period, 21.2% of Maryland homes had price drops — up from 20% the prior year. Homes are selling for 99.4% of list price, down 0.65 points year-over-year.

For buyers, this means something specific: you are no longer making decisions in 24–48 hours on a home you've toured once. You have time to schedule a second showing, get a full inspection, do neighborhood research, and negotiate calmly. The panic-buying environment of 2021–2022 — where buyers waived inspections, waived appraisals, and wrote cover letters begging sellers to choose them — is gone in this market. This is the most significant quality-of-life improvement in the buying experience that this area has seen since the pandemic.

Force 4: Prices Are Stable, Not Falling — Which Is Actually Good News

One of the most common questions I get is: 'Should I wait for prices to fall?' The honest answer is: meaningful price declines are not what the data supports, and waiting for them is a strategy that has cost DC and Maryland buyers real money over the past decade.

At the statewide Maryland level, the February 2026 median sale price of $427,000 represents a 2.9% year-over-year increase (Redfin). The Bright MLS 2026 forecast projects the Mid-Atlantic region median to rise 2.6% in 2026. The Jamil Brothers Maryland seller guide (January 2026) projects 2–4% statewide appreciation. These are modest, sustainable growth rates — not the 15%+ annual spikes of 2021–2022, and not a crash.

Why is stable appreciation good news for buyers? Because it means the market is predictable. When you buy in a market with 2–4% projected annual appreciation, you can make a financially rational decision: you know roughly what your asset will be worth in five years, you can calculate your equity buildup, and you can compare that to the cost of renting over the same period. That predictability is far more valuable for planning purposes than a volatile market where prices might drop 10% or jump 20%.

Maryland home prices currently sit approximately 80% above their pre-pandemic levels. That structural appreciation represents real, accumulated homeowner equity — and it's also a signal that the fundamentals supporting this market (employment, population, limited land) remain intact. The conditions that created the 2008 crash — loose lending, widespread speculation, subprime mortgages — are simply not present in this market today.

Force 5: Federal Workforce Uncertainty Is a Real Factor — Concentrated in DC, Limited in Maryland

I've covered this in depth in Post 3 of this series (What Federal Employees and Contractors Need to Know), but it deserves a direct answer here: yes, federal workforce uncertainty is affecting the DC market, and no, it is not affecting all of the markets we serve equally.

Washington DC proper is absorbing the most impact: active inventory up 50%+, median days on market rising, and the Bright MLS 2026 forecast projects DC as the only Mid-Atlantic market with a projected price decline (approximately -1%). This is partly federal workers listing homes, partly federal-adjacent buyers pausing purchases, and partly the ripple effect of uncertainty on market sentiment.

Montgomery County and Prince George's County are more insulated: Both counties have more diversified employment bases — biotech, health care, university employment, private sector — and while the federal employment impact is visible in some data (days on market increasing, some price softening), neither county is experiencing the kind of disruption visible in DC proper. Bright MLS projects the broader Mid-Atlantic to see a 2.6% price increase in 2026, and Montgomery County's fundamentals (strong schools, limited supply, Red Line access) remain structurally sound.

If you are a buyer with stable, non-federal employment, the federal uncertainty is working in your favor: it's contributed to the inventory increase and the seller flexibility that is currently creating buying opportunities. The market disruption is someone else's problem — and your opportunity.

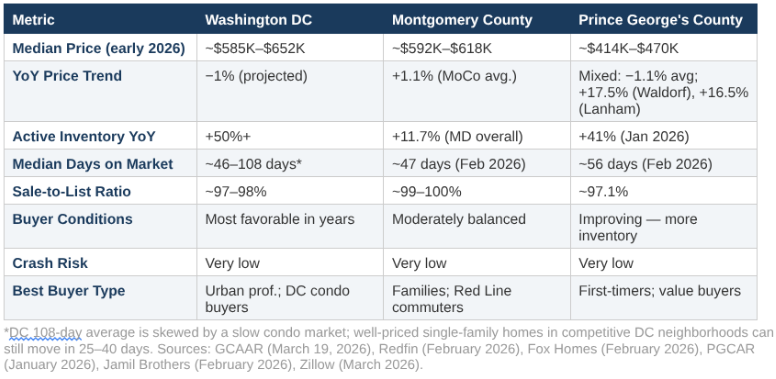

Market by Market: The Data for Your Specific Target Area

Here's the jurisdiction-by-jurisdiction breakdown as of March 2026, with current data from the most recent GCAAR, Redfin, Bright MLS, and PGCAR reports:

Washington DC: The Most Disrupted Market — and a Real Buyer Window

DC proper is the most interesting market in the region right now — and not in a bad way, if you're a buyer. The combination of rising inventory (50%+ year-over-year), slower sales (median days on market up to 47+ days in February per GCAAR), and a projected 1% price decline creates a genuinely different buying environment than any DC buyer has experienced since before the pandemic.

The DC condo market is bearing the most pressure. Condos are sitting longer, price drops are more common, and buyers are getting seller credits and concessions on condo purchases with a regularity that hasn't existed in years. If you're a buyer targeting a DC condo — whether as a primary residence or an investment — spring 2026 is the most buyer-friendly condo window in recent memory.

Single-family rowhouses and townhomes in premium DC neighborhoods — Capitol Hill, Brookland, Petworth, Columbia Heights — are more resilient, though even these are selling slower than a year ago. The key distinction: well-priced homes in established, in-demand neighborhoods are still moving. Overpriced homes or those in neighborhoods with less clear demand are sitting.

My honest read for DC buyers: if you've been waiting to get into DC proper and your employment situation is stable (or non-federal), this is the strongest window in five years. The inventory increase is real, the competition has meaningfully reduced, and sellers in DC are negotiating in ways they weren't 18 months ago.

Montgomery County: Stable and Measured — With Pockets of Real Opportunity

Montgomery County sits in an interesting position in spring 2026: more balanced than its recent history, but still fundamentally a seller-adjacent market in premium neighborhoods. The Jamil Brothers February 2026 Montgomery County market report puts the median price at approximately $618,000–$625,000, with modest year-over-year appreciation of about 1.1%. The GCAAR February 2026 data shows median days on market at 47 days for the Montgomery County / DC area combined — up 161% year-over-year. Redfin January 2026 data shows 533 homes sold in Montgomery County, up from 517 in January 2025.

What this means in practice: Montgomery County is not the frenzy market it was in 2021–2022. Buyers who were previously shut out by 12-offer situations are now getting second showings, having conversations about repairs, and in some cases negotiating price. But supply is still tight — approximately 2.6 months county-wide per GCAAR — and well-priced homes in Bethesda, Silver Spring, and Rockville don't sit long. The market requires preparation and decisiveness; it just no longer requires waiving your rights to secure a home.

The neighborhoods with the most buyer leverage right now: up-county Gaithersburg and Germantown, where days on market are longer and seller flexibility is highest. The neighborhoods with the least buyer leverage: Bethesda, Chevy Chase, and North Potomac, where demand from high-income buyers (both federal-adjacent and private sector) keeps competition real.

Spring 2026 is a transitional moment for Montgomery County: still a seller-favorable market in premium areas, but with the most buyer leverage in years across the mid-tier price range ($400K–$650K). Buyers who come prepared with pre-approvals and clear neighborhood priorities are closing deals with seller credits and repair concessions that were unthinkable in 2022.

Prince George's County: The Most Complex Story — and the Most Compelling Value

Prince George's County presents the most nuanced picture in the region, and it requires hyperlocal analysis rather than county-wide averages. The PGCAR January 2026 market report is the clearest data point: active listings are up 41% year-over-year, pending sales grew 4.5% month-over-month, and homes are selling at 97.1% of original listing price. Inventory growth is improving buyer options while demand remains strong enough to keep prices stable.

The neighborhood-level data from Fox Homes (February 2026) tells the most important story: within a single county, you have Waldorf up 17.5% year-over-year, Lanham up 16.5%, Brentwood up 15.6%, and Mount Rainier up 13.4% — while other neighborhoods like Bladensburg (-32%), Greenbelt (-24.6%), and Suitland (-17.8%) show significant declines. That's not a county in distress; that's a market with dramatic internal variation driven by buyer preference, Metro access, and neighborhood investment levels. The declining areas reflect transaction mix shifts and specific supply dynamics, not broad market weakness.

For buyers, this has one clear implication: in Prince George's County, the neighborhood decision is more consequential than in any other market we serve. The difference between buying in Mount Rainier (up 13%) and Bladensburg (down 32%) isn't a difference in county — it's a difference in specific location choices that local market knowledge can guide. This is the market where working with an agent who knows the specific blocks, not just the zip codes, matters most.

The fundamental case for PG County buyers in 2026 remains what it's been: the most accessible entry point into the DC metro area, with meaningful upside in specific neighborhoods that are being discovered by buyers priced out of DC and Montgomery County. The 41% active listing increase means more choice than the county has offered buyers in years. And the Purple Line light rail — connecting PG County communities to Bethesda when completed — is infrastructure investment that will be priced in fully once it opens.

Should You Wait for a Better Time to Buy?

This question deserves a direct answer, because 'wait for the right time' is advice that has cost DC and Maryland buyers real wealth over the past two decades.

The three most common reasons buyers in this market tell me they're waiting, and my honest response to each:

'I'm waiting for rates to come down further.'

Rates are projected to ease modestly — from 6.1% today to perhaps 5.9%–6.15% by year-end. That's a monthly savings of approximately $50–$100 on a $500,000 loan. In the same period, if Maryland prices appreciate at the projected 2–4% rate, a $500,000 home becomes a $510,000–$520,000 home. You've saved $600–$1,200 in interest and spent $10,000–$20,000 more on the purchase. The math does not favor waiting for rate improvements in a market with projected appreciation.

The one exception: if you're currently in a financial position that wouldn't qualify you at today's rates — and a modestly lower rate would make the difference — then waiting for that rate improvement while you build savings makes sense. The issue is financial readiness, not market timing.

'I'm waiting for prices to fall.'

No major forecaster is projecting meaningful price declines in the Maryland suburbs in 2026. The Bright MLS, Redfin, Jamil Brothers, and Houzeo forecasts all point to 1–4% appreciation statewide. DC proper has a projected -1% price movement — not a crash. Home prices in Maryland currently sit 80% above pre-pandemic levels, supported by structural demand fundamentals that aren't going away: limited land, strong employment, and persistent population growth in the region.

Waiting for a price drop that isn't forecast — while continuing to pay rent that has risen 20–40% since 2019 in this market — is not a financial strategy. It's a delay with a real cost.

'I'm waiting until the federal situation settles down.'

This is the most reasonable version of 'waiting' in the current environment, and it applies specifically to federal employees and contractors with genuine employment uncertainty. If your employment situation is the source of uncertainty, waiting for it to resolve before committing to a purchase is prudent. But if you're a private-sector buyer, a buyer with stable non-federal employment, or a federal buyer whose position is secure — you're waiting for someone else's uncertainty to resolve before acting on your own clearly favorable situation. That doesn't make financial sense.

The buyers who have consistently built the most wealth in this market are not the ones who timed the bottom. They're the ones who bought when they were ready, stayed for the long term, and let appreciation compound. The best time to buy was 10 years ago. The second best time is when you're financially and personally prepared to do it well.

Who Should Buy Now — and Who Should Wait

Let me be direct about which buyer profiles are best served by acting in spring 2026 versus waiting:

Spring 2026 is the right window if:

Your employment is stable — you have career tenure, a firm offer, or non-federal private sector income — and your timeline in the area is five or more years

You've been sitting on the sidelines waiting for conditions to improve and this is objectively the most improved conditions since 2019

You're targeting DC proper and have been waiting for the competitive frenzy to subside — the inventory surge and rising days on market represent your window

You're a first-time buyer in Prince George's County who wants to get in before the Purple Line infrastructure is fully priced in

You have 10–20% down payment ready and a fully underwritten pre-approval in hand — you're prepared to move when the right property appears

You're a move-up buyer in Montgomery County — the longer days on market are making it easier to sell your current home with a contingency, something that was nearly impossible two years ago

It makes sense to wait if:

You are a federal employee with genuine, unresolved employment uncertainty — probationary status, an agency under active restructuring, or a buyout offer you haven't decided on

Your down payment or reserves aren't where they need to be — buying undercapitalized in any market is a risk that outweighs the benefit of buying now

You haven't visited the area and don't yet know which neighborhood fits your lifestyle and commute — renting for 6–12 months to gather that information is a smart investment

Your credit score is in a range that would qualify you for meaningfully better rates with 6 months of improvement — the rate benefit of improving from 680 to 740 is more valuable than any near-term market timing

Frequently Asked Questions

Q: Will DC and Maryland home prices fall in 2026?

In Washington DC proper, a modest -1% price decline is projected by Bright MLS — making it the only Mid-Atlantic market expected to see any price softening. In the Maryland suburbs, 2–4% appreciation is the consensus forecast, with statewide Maryland data from Redfin showing a 2.9% year-over-year increase in February 2026. A broad price crash is not supported by any credible forecast for this market: inventory is still below balanced-market levels, lending standards are sound, and the employment base remains structurally diverse.

Q: How competitive is the DC and Maryland market for buyers right now?

Significantly less competitive than 2021–2022, but not a buyer's market. The median days on market in Montgomery County and DC reached 47 days in February 2026 — up 161% year-over-year — and Maryland supply sits at approximately 2.6 months, above the five-year average of 1.8 months. Well-priced, well-maintained homes in desirable locations still receive multiple offers. But overpriced homes are sitting, and buyers are successfully negotiating seller credits, repair allowances, and below-asking prices on non-premium inventory with much greater frequency than in prior years.

Q: What are the best DC and Maryland neighborhoods to buy in right now in 2026?

It depends on your budget and situation, but the neighborhoods with the strongest combination of value, buyer leverage, and long-term upside right now are: Silver Spring and Rockville (Montgomery County) for buyers in the $400,000–$600,000 range who want Red Line access and strong schools; Mount Rainier, Brentwood, Hyattsville, and the New Carrollton corridor in Prince George's County for buyers seeking close-in value with Metro access and appreciation trajectory; and Petworth, Brookland, and Brightwood in DC proper for buyers with stable employment who want the DC urban experience at a lower price point than Capitol Hill.

Q: Is the DC area housing market going to crash because of federal layoffs?

No credible forecast projects a crash. The federal workforce reduction is real and is affecting DC proper's market more than the Maryland suburbs — but the DC metro employment base is large and diverse enough that even a significant federal reduction doesn't create the systemic conditions for a market crash. Maryland home prices sit 80% above pre-pandemic levels, lending standards are sound, homeowner equity is historically high, and inventory — while rising — is still below balanced-market levels. What federal uncertainty has created is a more favorable environment for prepared buyers; it has not created a market in distress.

Q: When is the best time of year to buy in DC and Maryland?

Spring (March through June) is when the most inventory hits the market — which gives buyers the most options but also the most competition. Fall (September through November) and winter (December through February) typically have less competition and more motivated sellers, but also fewer properties to choose from. In the current environment, spring 2026 is unusual: inventory is high enough that the typical spring competition dynamic is somewhat muted, making it an unusually good spring buying window. The best time to buy is ultimately when you're prepared and the right property is available — not a specific calendar month.

Q: How much have DC and Maryland home prices increased since before the pandemic?

Maryland home prices currently sit approximately 80% above their pre-pandemic (early 2020) levels, according to Houzeo and multiple MLS-based analyses. This appreciation represents the strongest argument against waiting for a meaningful price correction: the structural fundamentals — employment, demand, limited supply — that drove that appreciation haven't changed. DC proper has seen the highest absolute appreciation in the region during this period, though it is now experiencing the most normalization. The Maryland suburbs have appreciated more steadily and with less volatility.

The Bottom Line: What the Data Says

The DC and Maryland market in spring 2026 is not what it was in 2021, and it's not what the most alarming headlines suggest. The honest read of the data is this: inventory is rising, sellers are flexible, homes are sitting longer, and buyers who arrive prepared are executing transactions with leverage that hasn't been available in years.

Whether 2026 is a good time to buy in this specific market depends on your employment stability, your five-year plan, your financial readiness, and which specific neighborhood you're targeting. The aggregate data is favorable. Your individual situation is what determines whether you act on it.

If you want a straight assessment of where things stand in the specific neighborhoods you're considering — and an honest answer to whether right now is the right time for your situation — that's exactly what I do. The consultation is free, and I'll give you the same data-driven analysis I've put into this article applied to your specific circumstances.

Thinking About Buying in DC or Maryland in 2026?

The data in this article gives you the big picture — but the right move depends on your specific situation, budget, and timeline. In a free 30-minute consultation, I'll give you a street-level read on where things stand in the specific neighborhoods you're targeting, and tell you honestly whether right now is the right time for you.

Call or text Ryan Hehman | 443-990-1230

Free consultation. No obligation. Honest guidance.

Related articles on this site:

Relocating to Washington DC & Maryland: The Complete 2026 Guide from a Local Expert

DC vs. Maryland Suburbs: Where Should You Actually Live When Relocating to the DC Area?

Is It Better to Rent First or Buy Immediately When Moving to the DC Area?

What Federal Employees and Contractors Need to Know About Buying a Home in DC and Maryland Right Now

How to Buy a Home in DC or Maryland Before You Move: A Step-by-Step Guide for Out-of-State Buyers