Is It Better to Rent First or Buy Immediately When Moving to the DC and Maryland Area?

If you're relocating to the Washington DC and Maryland area and trying to decide whether to rent first or buy immediately, here's the short answer: if your employment is stable, you plan to stay at least five years, and you've done enough research to know which area you want to be in, buying immediately is almost always the stronger financial move. If you're uncertain about your job situation, haven't visited the area, or your timeline is short, renting first is the smarter hedge — even at this market's rental prices.

Neither choice is wrong. But this decision deserves more than a coin flip, and the answer looks different for a federal employee with employment uncertainty than it does for a private-sector family with a firm five-year plan. This article gives you the data and the framework to make the right call for your specific situation.

I'm Ryan Hehman, a real estate agent serving Washington DC and the Maryland suburbs — primarily Montgomery County and Prince George's County. I talk through the rent-versus-buy question with nearly every relocation client I work with, and I don't have a financial stake in which choice you make. What I do have is a clear read on what the numbers actually look like in this specific market right now.

What Renting Actually Costs in DC and Maryland in 2026

The first thing most relocation buyers don't fully account for is just how expensive renting is in this market. The DC metro area has some of the highest rents in the country, and the Maryland suburbs are no longer the relative bargain they once were.

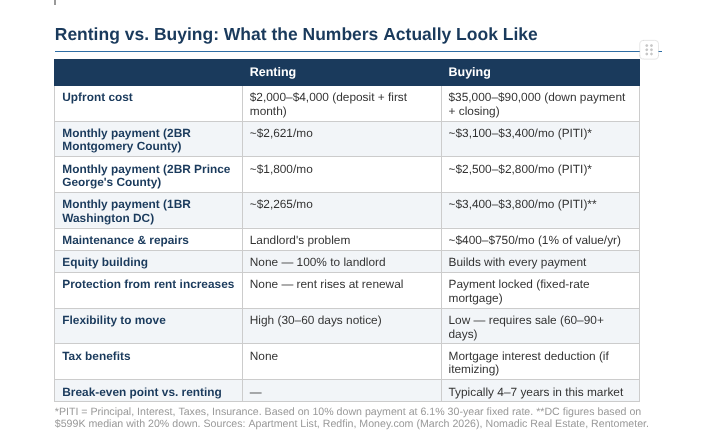

Washington DC: The average one-bedroom apartment in DC rents for approximately $2,265 per month. A two-bedroom averages $3,200–$3,500 in most desirable neighborhoods. And critically, DC's rents have been nearly flat since 2019 — which is a genuinely unusual situation in a market where surrounding suburbs have seen 20–40% rent increases over the same period.

Montgomery County: Average rent for a one-bedroom is approximately $2,094 per month. Two-bedrooms average $2,621. The gap between DC and Montgomery County rents has collapsed dramatically — DC used to cost $280–$300 more per month than Montgomery County in 2017–2019. That premium is now just $63. In practical terms, renting in the Maryland suburbs is no longer the clear deal it once was compared to living in the city.

Prince George's County: The most affordable rental option of the three. Average one-bedroom rents run approximately $1,500–$1,800 per month; two-bedrooms come in around $1,800–$2,100. This is the market where renting still provides meaningful savings relative to buying on a monthly basis — though appreciation trends in specific PG County neighborhoods are starting to narrow that gap.

The 'rent is throwing money away' argument is oversimplified — but so is the argument that renting is always the smarter move. In the DC and Maryland market specifically, monthly rent costs are high enough that the financial case for buying is stronger than in many other cities.

One data point that surprises most relocation buyers: every single jurisdiction surrounding DC — without exception — has seen double-digit rent increases since 2019. Frederick County, Maryland is up 41%. Prince William County is up 34%. Loudoun County is up 29%. The DC metro is not a rental market that offers long-term price stability. Renters are subject to increases at every lease renewal, and those increases have been real and sustained.

The table above makes one thing obvious: buying costs more on a monthly basis, especially upfront. At current mortgage rates of approximately 6.1% for a 30-year fixed loan (as of mid-March 2026), the monthly payment on a median-priced Montgomery County home with 10% down is going to be meaningfully higher than the equivalent rental. That monthly gap is real and shouldn't be minimized.

But the comparison doesn't end at month one — and this is where most rent-versus-buy analyses go wrong. The right question isn't 'which is cheaper per month?' It's 'which builds more wealth over my actual time horizon?'

The Break-Even Timeline: When Does Buying Start to Win?

The break-even point is the moment when the total cost of buying (including your down payment, closing costs, mortgage payments, maintenance, and eventually transaction costs to sell) equals what you would have spent renting. After that point, owning is building real wealth.

In the DC and Maryland market, the break-even point for buying versus renting typically falls between four and seven years, depending on your specific purchase price, down payment, and which area you're in. Here's why that range exists:

In Prince George's County — where purchase prices are lower and rent isn't as elevated — the monthly gap between renting and buying is smaller, and break-even can come in closer to four to five years.

In Montgomery County — where purchase prices are higher but rents are also substantial — break-even typically falls around five to six years.

In DC proper — where purchase prices are highest relative to rents, and the price-to-rent ratio is approximately 24x — the break-even timeline extends to five to seven years for most buyers.

What happens after break-even? This is where the compounding effect of homeownership becomes real. With each monthly mortgage payment, you're building equity through principal paydown. And if home values appreciate — which they historically do in this market — that equity compounds further. Bright MLS projects modest rent gains of 1.5–3.8% annually in the Maryland suburbs for 2026. That means every year you're renting, your housing costs are rising. Every year you're in a fixed-rate mortgage, your payment stays exactly the same.

At a 2% annual appreciation rate on a $500,000 home, you're gaining $10,000 in value per year — completely passively. At 3% appreciation, that's $15,000. Over five years, that's $50,000–$75,000 in equity growth that a renter never sees.

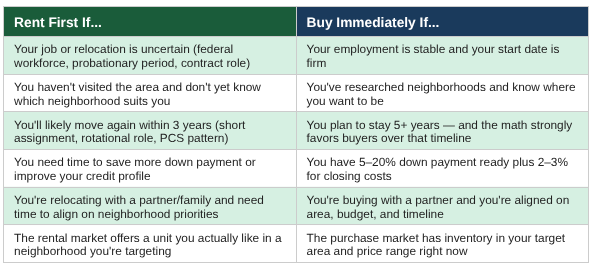

The Five Relocation Scenarios: Which One Is Yours?

After walking dozens of relocation clients through this decision, I've found most people fall into one of five situations. Here's how I'd think about each one:

Scenario 1: Stable job, five-plus year plan, know the area → Buy immediately

If you've visited the area, know which neighborhood you want, have a firm job with stable income, and intend to stay for at least five years, buying immediately is the right call in almost every case. The monthly payment will likely be higher than comparable rent, but the wealth-building differential over five years is significant. You're also protecting yourself from rent increases, building equity, and getting the benefit of any appreciation.

The only thing that changes this calculus is inventory. If there's limited supply in your target neighborhood right now, renting for three to six months while you wait for the right property to come on the market can be a reasonable bridge — not a long-term hedge.

Scenario 2: Federal employee or contractor with employment uncertainty → Rent first

I'll be direct here because I think some agents aren't: if you're a federal employee navigating genuine uncertainty about your position, renting first is the responsible choice. The DC market has seen a notable increase in inventory partly because some federal employees are hedging their housing decisions — and that's not irrational.

Renting for six to twelve months gives you time to see how your employment situation resolves while still getting settled in the area. It's not a permanent state. If your situation stabilizes and you decide to buy after a year of renting, you'll have the benefit of knowing the neighborhoods from the inside and buying with confidence rather than urgency.

If you're a federal employee considering buying right now, the right question to ask yourself is: 'If I lost this job, could I cover this mortgage for three to six months while I found another one?' If the answer is yes — you have reserves, marketable skills, and a clear employment picture — buying may still make sense.

Scenario 3: Military family on PCS orders → Depends on your timeline and VA eligibility

PCS buyers have the advantage of VA loan eligibility, which eliminates the down payment barrier entirely and keeps closing costs lower than conventional financing. For military families with a three-year or longer assignment — or who intend to keep the property as a rental when they eventually PCS again — buying often makes excellent financial sense.

For families with a shorter assignment or genuine uncertainty about the next duty station, renting first preserves flexibility. The DC area rental market has enough inventory that military families can find good temporary housing without locking into a lease that's hard to exit.

Scenario 4: First-time buyer, limited down payment → Explore programs before deciding

If you're a first-time buyer with a limited down payment, the rent-versus-buy decision may actually be made for you by your current financial position. The good news: Maryland has several programs specifically for first-time buyers that can meaningfully change the math.

The Maryland Mortgage Program offers competitive rates and down payment assistance to eligible first-time buyers. Montgomery County and Prince George's County both have local assistance programs as well. A conversation with a local lender who knows these programs is worth having before you assume you can't afford to buy — I've seen buyers get into homes with as little as 3.5% down when they didn't think homeownership was within reach.

Scenario 5: Remote or hybrid worker with location flexibility → Take more time to research

If you're relocating without a fixed office address — or with a hybrid schedule that doesn't anchor you to a specific commute corridor — the rent-first approach has real merit. The DC and Maryland area has enough neighborhood variation that choosing the right one is genuinely important to your daily quality of life, and that's harder to assess from outside the market than it is after you've lived here for six months.

Renting in a neighborhood you're seriously considering before buying there is one of the best due-diligence moves a relocation buyer can make. You'll know whether the commute is actually as manageable as Google Maps suggested, whether the neighborhood fits your lifestyle, and which specific streets and blocks you'd want to be on — all of which makes your eventual purchase significantly better.

A Word About Waiting: The Hidden Cost of Staying on the Sidelines

There's a version of the rent-first decision that starts as a reasonable hedge and turns into an indefinite delay — waiting for rates to drop, waiting for prices to fall, waiting for the 'right time.' I want to address that directly.

As of mid-March 2026, the 30-year fixed mortgage rate is approximately 6.1% — down from a peak above 7% in late 2024. Major forecasters including the Mortgage Bankers Association project rates to hold in the low-to-mid 6% range for most of 2026. Most economists do not expect a return to the emergency-era rates of 2020–2021. The long-run Freddie Mac average since 1971 is approximately 7.8%. By historical standards, 6% is not a bad rate to borrow money.

Meanwhile, prices in Montgomery County and Prince George's County continue to appreciate at 2–4% annually, with specific PG County neighborhoods running significantly higher. A $475,000 home today at 3% annual appreciation is a $490,225 home in twelve months. That's $15,225 in additional purchase price — which raises your down payment requirement and your loan size, and typically more than offsets any benefit from a mildly lower rate.

Waiting for the 'perfect moment' to buy in this market has cost buyers real money over the past decade. The buyers who came out ahead weren't the ones who timed the market — they were the ones who bought when they were ready, held the property, and let appreciation do its work.

The one genuinely valid reason to wait: if your personal financial situation — employment stability, credit score, down payment savings — isn't where it needs to be. Those are fixable problems worth addressing. Market timing is not a reliable strategy in this market or any other.

If You Do Rent First: How to Do It Strategically

Choosing to rent first isn't a failure — it's a strategy. But it's only effective if you use the rental period intentionally. Here's how I coach clients who decide to rent first:

Rent in the neighborhood you're seriously considering buying. Don't rent in Silver Spring if you think you want to buy in Rockville. The point of renting first is to validate your neighborhood hypothesis from the inside.

Set a firm timeline. 'Rent for a year then decide' is fine. 'Rent indefinitely until things feel right' is a trap. Decide in advance when you'll make your buying decision and commit to that date.

Use the rental year to get your finances in order. Shore up your credit score, add to your down payment savings, and get a mortgage pre-approval completed before your lease ends. When your year is up, you want to be ready to move fast.

Stay in close contact with a local agent. Markets shift. Neighborhoods evolve. The home that wasn't on the market when you arrived may be available six months later. Having an agent who knows what you're looking for means you don't miss the right opportunity because you weren't paying attention.

Be aware of lease terms. Most DC and Maryland landlords require 12-month leases with 60-day notice to vacate. Build your buying timeline around that — so you're not stuck in a lease when you find the right home.

Frequently Asked Questions

Q: Is it cheaper to rent or buy in the DC and Maryland area in 2026?

Month-to-month, renting is almost always cheaper upfront in this market. A two-bedroom rental in Montgomery County averages $2,621/month; the equivalent owned home would carry a PITI payment of $3,100–$3,400 depending on your down payment. But over a five-year horizon, buying builds tens of thousands in equity through principal paydown and appreciation — and locks in your housing cost while rents continue to rise. Which is 'cheaper' depends entirely on how long you're staying.

Q: How long do I need to stay in the DC area for buying to make financial sense?

The break-even point in this market is typically four to seven years, depending on purchase price, down payment, and which area you're buying in. Prince George's County's lower prices and improving appreciation trends put break-even closer to four to five years. Montgomery County and DC proper are more in the five-to-seven-year range. If your assignment or life plan has you in the area for at least five years, buying almost always wins on the numbers.

Q: What are current mortgage rates in DC and Maryland?

As of mid-March 2026, the 30-year fixed mortgage rate is approximately 6.1%, per Freddie Mac's most recent weekly survey. This is down from a peak above 7% in late 2024. Most major forecasters project rates to hold in the 6.0%–6.5% range through the remainder of 2026, with possible modest improvement in the second half of the year if inflation continues to moderate. VA loan rates tend to run slightly lower — typically 5.7%–6.0% for eligible buyers.

Q: Should I rent first if I'm not sure which neighborhood I want?

Yes — if you genuinely don't know which area suits your lifestyle and commute, renting first is a smart move. The DC and Maryland area has enough neighborhood variation that choosing the wrong one is a real and costly mistake. Renting for six to twelve months in your target area before buying gives you ground-level information that no amount of Zillow browsing can replace. Use that time intentionally: commute from different points, explore on weekends, and talk to neighbors.

Q: What down payment do I need to buy in DC or Maryland?

Conventional loans require as little as 3–5% down for first-time buyers, though putting down 20% eliminates private mortgage insurance (PMI) and meaningfully reduces your monthly payment. VA loans for eligible veterans and military buyers require zero down payment. FHA loans allow 3.5% down with a credit score of 580 or above. Maryland's Mortgage Program offers additional down payment assistance for eligible buyers. At a $475,000 purchase price, 10% down is $47,500; 20% down is $95,000. Closing costs in Maryland typically add another $8,000–$15,000 on top of the down payment.

Q: Is the DC housing market going to crash in 2026?

No major forecaster is projecting a crash in the DC metro area in 2026. Bright MLS projects performance ranging from a modest price dip in DC proper (driven by federal workforce uncertainty and rising inventory) to 2–3% appreciation in the Maryland suburbs. The underlying demand fundamentals — federal employment, biotech, tech sector, and institutional demand — remain strong. A 'crash' scenario would require a dramatic national economic disruption, not the current conditions of moderating appreciation and normalizing inventory.

The Bottom Line

Renting first is the right call when your situation has genuine uncertainty — employment, timeline, or neighborhood knowledge. Buying immediately is the right call when you're stable, settled on your area, and planning to stay long enough for the numbers to work in your favor.

In the DC and Maryland market, the case for buying is stronger than in most cities — because rents are high, appreciation has been real and sustained, and the employment base that drives this market is structurally durable. But no one should buy a home before they're ready, and 'ready' means emotionally, financially, and informationally prepared.

If you're still not sure which path is right for your situation, that's the exact conversation I have with every new relocation client — and it's one I'm happy to have with you, at no cost and no obligation.

Not Sure Whether to Rent or Buy? Let's Run Your Numbers.

Every relocation situation is different. In a free 30-minute call, I'll help you figure out whether renting or buying makes sense for your specific timeline, budget, and situation — and if buying makes sense, I'll help you find neighborhoods that could be a good fit for you and what to expect from the market right now.

Call or text Ryan Hehman | 443-990-1230 | Email: Ryan.Hehman@compass.com

Free relocation consultation. No obligation. No pressure.