What Federal Employees and Contractors Need to Know About Buying a Home in DC and Maryland Right Now

If you're a federal employee or government contractor trying to decide whether to buy a home in the Washington DC and Maryland area right now, the honest answer is: it depends on one question more than any other — how secure is your job? If your position is stable, your income is reliable, and you plan to stay in the area for five or more years, buying in this market still makes strong financial sense, and the current environment is actually creating opportunities that didn't exist eighteen months ago. If you have real uncertainty about your employment situation — probationary status, a program under active review, or a buyout offer on the table — renting first is the more prudent call.

I'm not going to pretend this is a normal market for federal buyers. It isn't. The federal workforce reductions that began in early 2025 have had a measurable effect on housing activity in the DC metro area, and any agent who tells you otherwise isn't paying attention. But 'measurable effect' is not the same as 'market collapse,' and a clear-eyed read of the actual data tells a more nuanced story than the headlines suggest.

I'm a real estate agent serving Washington DC and the Maryland suburbs — primarily Montgomery County and Prince George's County. I've worked with federal employees and contractors throughout my career, and I've been watching this market closely through the current uncertainty. This article gives you the real picture — the data, the honest risk assessment, and a clear framework for making the right decision for your specific situation.

The State of the DC and Maryland Market for Federal Buyers Right Now

Let's start with the data, because it's more nuanced than either the alarm bells or the reassurances you've likely been hearing.

The impact is real but uneven. A Bright MLS survey found that nearly 40% of DC-area agents had worked with a client whose decision to buy or sell was directly related to federal workforce reductions. More than a third of agents reported that layoffs were causing prices in their local markets to fall. DC proper is bearing the brunt: inventory in Washington DC is up over 50% year-over-year, well above the 30% national average, and median home prices are projected to see a modest 1% decline in 2026 — making it the only Mid-Atlantic market expected to see any price softening this year.

The Maryland suburbs are holding. Montgomery County and Prince George's County are demonstrating considerably more resilience. Montgomery County prices have shown modest appreciation of about 1.1% year-over-year, homes are selling in approximately 39 days, and the Bethesda-Rockville-Silver Spring corridor continues to attract both federal and private-sector buyers. Prince George's County presents a mixed picture county-wide, but specific neighborhoods — Glenn Dale, Takoma Park, Hyattsville — have seen double-digit appreciation, and the county median remains one of the most accessible entry points in the entire metro area.

Buyer hesitation is creating real opportunity. Here's the data point most federal buyers aren't hearing: homes that have been sitting on the market for more than two weeks are now yielding lower sale prices and seller credits with meaningful frequency. Exclusive buyer agents in the market are consistently negotiating below asking price on non-premium inventory. The buyers who are well-prepared and clear-eyed about their situation are finding leverage that simply didn't exist in 2022 or 2023.

The DC metro area has over 500,000 federal workers and hundreds of thousands more government contractors. Not all of them are at risk, not all at-risk employees will leave, and the private sector employment base that co-anchors this market — biotech, defense contractors, tech, health care — has not been affected by the federal reductions. This is a disrupted market, not a broken one.

What Is Actually Happening: Four Facts the Headlines Miss

Fact 1: The federal workforce reduction is large but the regional economy is much larger

The DC metro area is home to more than 6 million residents and has an exceptionally diversified economy. Federal employment accounts for nearly 1 in 5 workers in the immediate area — but that leaves 4 in 5 workers employed outside the federal government, in sectors including biotech and life sciences (NIH, FDA, and dozens of private firms along the I-270 corridor), defense contracting, cybersecurity, legal and lobbying, health care, education, and technology. Several counties in Maryland rank among the top 10 highest-income counties in the country by median household income. That structural economic diversity is exactly why real estate analysts are not forecasting the kind of collapse that followed, for example, the 2005 closure of major military bases in base-dependent communities.

Fact 2: The sellers leaving are creating opportunity for buyers who stay

Federal employees who accepted voluntary early retirement or buyout offers — particularly older, higher-income workers who owned homes — are listing those properties. This has pushed active inventory in DC up meaningfully and is beginning to show in the Maryland suburbs as well. For federal employees who are staying in the area and whose employment is secure, this inventory increase is a genuine buying opportunity. You're competing against fewer buyers for more properties, with sellers who are more motivated and more flexible than they were eighteen months ago.

One senior Bright MLS economist noted that 'federal buyouts provided older, often higher-income homeowners a chance to cash out and relocate,' and that the ripple effects would likely continue through 2026. For stable buyers, that means more to choose from and more room to negotiate.

Fact 3: Buyer hesitation is a market signal, not just a personal feeling

The data shows that new pending sales in the DC area were down about 3.3% from a year earlier — essentially matching broader regional trends and suggesting the federal layoff effect isn't as isolated as some assume. That said, some buyers who had active contracts rescinded them when probationary jobs were revoked, and others paused searches out of general uncertainty. This buyer hesitation, paradoxically, is what's creating a window for buyers who are confident in their situation. The buyers who get pre-approved, clarify their employment picture, and move decisively are operating in a market with real leverage on their side.

Fact 4: The 2026 federal pay situation has reduced buying power for some employees

One detail that hasn't gotten enough attention: the 2026 federal pay raise was just 1% — applied entirely to base pay, with no increase in locality pay. For the Washington-Baltimore-Arlington locality, the locality adjustment remained frozen at 33.94% from 2025 levels. This means that in real terms, federal employees in the DC area received a pay increase well below inflation for the second consecutive year — and their buying power relative to home prices has declined modestly. At GS-12 and GS-13 levels, the dollar increase from the 1% raise was approximately $800–$1,000 annually, which does not meaningfully change mortgage qualification. But it's a real factor in long-term affordability planning, and worth acknowledging honestly.

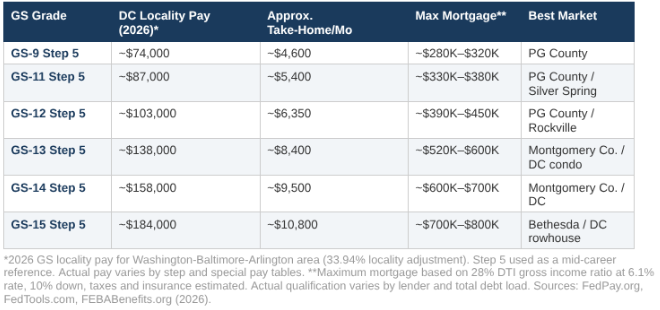

What Federal Pay Actually Buys in This Market: GS Grade to Buying Power

This table gives federal employees a realistic picture of buying power at each GS grade in the DC-Maryland market, assuming the Washington-Baltimore-Arlington locality adjustment. All figures assume a 6.1% 30-year fixed mortgage rate and a standard 28% front-end debt-to-income ratio.

A few important observations from this table:

GS-9 through GS-11 employees face a genuine affordability challenge in DC proper and Montgomery County's premium submarkets. The most accessible path to homeownership for these grade levels is Prince George's County, where a $300,000–$380,000 purchase price is achievable and the market has real upside.

GS-12 and GS-13 employees — the largest single cohort of federal workers in the DC area — can realistically access most of Montgomery County's mid-tier market and much of Prince George's County, though Bethesda and Chevy Chase remain out of reach at these income levels without significant down payment reserves or a dual-income household.

Dual-income federal households should calculate combined qualifying income. Two GS-12 incomes gives a household an approximately $200,000 annual income and buying power in the $750,000–$850,000 range — competitive in much of the market.

The frozen locality pay in 2026 doesn't change the mortgage math significantly at these grade levels, but it does mean your monthly payment will feel slightly more burdensome than it would have in a year with normal salary growth.

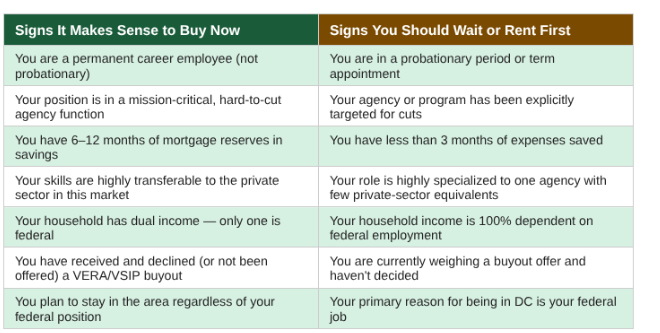

The Decision Framework: Should You Buy Now or Wait?

The most important thing I can tell you is this: the right answer is different for a permanent GS-14 career employee at NIH than it is for a probationary GS-11 at an agency currently under active restructuring. The following framework helps you assess your specific situation clearly.

The most important column in that table is the left one. If the majority of your answers fall on the left side, buying now makes sense and this market is offering you genuine opportunity. If the majority fall on the right, the honest recommendation is to rent for six to twelve months, let the employment picture clarify, and revisit with more confidence.

Here's the question I ask every federal buyer who's on the fence: 'If you lost this job, what would happen?' If the answer is 'I'd find another position in this market within a few months and could cover the mortgage in the meantime with savings,' that's a manageable risk. If the answer is 'I'd have to move and would need to sell quickly,' that's a different calculation — and renting first is the right call.

Why Now Is Actually a Strong Buying Window for Well-Positioned Federal Employees

If your employment situation is stable and you've been sitting on the sidelines waiting for conditions to improve, I want to make the affirmative case directly. The combination of factors in this market right now is genuinely favorable for prepared buyers in a way that hasn't existed since 2019.

Increased inventory means more choices and less competition

Active listings in DC are up over 50% year-over-year. Maryland inventory is up 16–24% depending on the area. Homes are sitting on the market longer — the median days on market in Maryland hit 60 days in January 2026, up 14 days from a year earlier. This is the kind of environment where you can make thoughtful decisions instead of panicked ones, and where sellers have moved away from the 'take it or leave it' posture of 2021–2022.

Sellers are more flexible than they've been in years

Agents consistently report successfully negotiating below asking price on non-premium inventory and securing seller credits toward closing costs or repairs. In early 2026, homes in DC are selling for approximately 97–98% of list price — still strong, but a meaningful shift from the 101–104% ratios that characterized the market two years ago. For buyers who come in prepared and make clean offers, there is real room to negotiate.

DC proper is offering a rare window in premium neighborhoods

This is the most counterintuitive point, and the one I think federal buyers are missing: DC proper's inventory surge and the modest 1% projected price decline mean that neighborhoods which were effectively impenetrable for normal buyers — parts of Capitol Hill, Logan Circle, some blocks in Petworth and Columbia Heights — are now seeing price reductions and extended market times on properties that simply would not have been available two years ago. For federal employees whose agencies are downtown and who have stable employment, this is a window that may not stay open long once uncertainty lifts.

Mortgage rates have improved and further easing is projected

The 30-year fixed rate as of mid-March 2026 is approximately 6.1%, down from above 7% in late 2024. Major forecasters including the Mortgage Bankers Association and Realtor.com project rates to average in the low-to-mid 6% range for most of 2026, with possible improvement in the second half of the year. This is not the 2.8% of 2021, but it's also not an outlier by historical standards — the long-run 30-year average since 1971 is approximately 7.8%.

The math is simple: a buyer who waits six months hoping for a better rate, and rates decline by 0.25%, saves approximately $50/month on a $500,000 loan. A buyer who waits and prices rise 2% in that period pays $10,000 more. Preparation beats timing.

Neighborhoods by Agency Location: Finding the Right Commute Anchor

Federal buyers have one practical advantage that civilian relocation buyers don't: a known, fixed workplace address. This makes neighborhood targeting significantly more precise. Here's how I think about the commute anchor for the most common federal employer locations in DC and Maryland:

Downtown DC Federal Triangle / L'Enfant Plaza / Capitol Hill campus employees

You have the broadest neighborhood options in the entire market because the Metro network radiates in every direction from downtown. DC proper neighborhoods — Capitol Hill, Brookland, Petworth — are your walkable, Metro-connected options. For Maryland, the Red Line to Silver Spring or Montgomery County and the Green Line to Prince George's County are both direct and reliable. Your commute from Silver Spring to Federal Triangle is approximately 25 minutes; from Hyattsville on the Green Line, roughly 20–30 minutes. The commute is genuinely manageable from a wide range of price points.

NIH / FDA / DHHS campus employees (Bethesda / White Flint / Rockville)

Your agency location anchors you firmly to the I-270 corridor and the Montgomery County Red Line. Bethesda offers walkability and proximity to campus but at premium prices ($900K+). Rockville and North Bethesda offer strong value with Red Line access at Rockville, White Flint, and Twinbrook stations in the $500,000–$700,000 range. For buyers stretching their budget, Gaithersburg and Germantown give you the most home for your money, with a MARC commuter rail option and access to campus via I-270 — though driving in rush hour on that corridor requires realistic expectations about commute time.

NSA / Fort Meade / Annapolis Junction employees

The NSA and surrounding contractor facilities sit between Baltimore and DC, which gives you a different geographic calculus. Prince George's County — Laurel, Beltsville, and College Park — offers the best combination of commute proximity, Metro access (Green Line to Greenbelt), and price point for NSA-area employees. Homes in this corridor in the $350,000–$480,000 range are genuinely available and have shown strong appreciation as remote-work flexibility has pushed buyers toward value markets.

USDA / FEMA / DHS campus employees (SW DC / Navy Yard / Suitland)

The Green and Yellow Lines serve this corridor well. DC's Southwest Waterfront and Navy Yard neighborhoods are expensive but have seen development investment that supports long-term value. Just across the DC line into Prince George's County, Seat Pleasant, Capitol Heights, and the communities near the Suitland Federal Center offer more accessible price points for employees who need to be in the southern Maryland / SE DC corridor

Specific Guidance by Employment Situation

Permanent career federal employees

If you hold a permanent, competitive service appointment with career tenure, you have the strongest position of any federal buyer in this market. Your job protection is meaningful — career employees cannot be summarily terminated without cause and due process — and your income is predictable. The main variable to assess is your agency's stability and whether a potential reassignment could affect your commute geography. If both of those check out, this market is offering you genuine buying opportunity.

Probationary employees (new hires or recent promotions)

This is the highest-risk category right now, and I'll be direct: if you are currently in a probationary period — typically the first year of a new appointment or promotion — buying a home during that window carries real risk in the current environment. Probationary employees have been disproportionately targeted in federal workforce reductions, and multiple reports confirm that buyers with probationary appointments have had purchase contracts rescinded after job loss. I recommend waiting until your probationary period has concluded and your career status is confirmed before making a purchase commitment.

Government contractors

Contractor risk is more nuanced and depends heavily on your contract vehicle, your agency customer, and your company's portfolio diversification. A contractor on a long-term IDIQ with a well-funded agency in a mission-critical function has a substantially different risk profile than one on a short-term task order with a small agency under active DOGE scrutiny. If your contract has been recently renewed, your company has diversified government and commercial revenue, and your customer agency is stable, contractor employment can be treated similarly to private-sector employment for home-buying purposes. If your contract renewal is uncertain or your company is heavily dependent on a single at-risk agency, the same caution I apply to probationary employees applies to you.

Employees who received or declined a VERA/VSIP buyout

If you were offered a buyout and declined, the fact that you made an active choice to stay carries real information. You've assessed your situation and decided your position is worth keeping. For most career employees in this situation, the buy decision analysis reverts to the normal framework: employment stable, timeline five-plus years, finances in order, buy. If you're still weighing a buyout and haven't decided, hold off on a home purchase until that decision is resolved.

If You Decide to Buy: Five Steps to Get It Right

For federal employees who've assessed their situation and decided buying makes sense, here's how to approach this market effectively:

Get a fully underwritten pre-approval, not just a pre-qualification. In this market, sellers and their agents want to see financing confidence, especially if you're competing against other offers. A fully underwritten pre-approval from a local lender who knows this market is significantly stronger than a quick online pre-qual. Disclose your federal employment and let the lender run your numbers with accurate current locality pay.

Be transparent with your lender about your employment situation. If there is any complexity — probationary status, a recent RIF, income from a buyout — your lender needs to know. Employment verification is a standard part of the mortgage process and lenders will check your job status before closing. Surprises at closing are avoidable if your lender has accurate information from the start.

Target your commute anchor, then work outward by budget. Use your agency's location as the starting point for your neighborhood search, then identify the Metro line that serves your workplace, and find neighborhoods along that line within your price range. This single approach eliminates hours of wasted research and touring in neighborhoods that won't work for your daily life.

Look seriously at homes that have been on the market for 15 or more days. In the current environment, properties that haven't gone under contract in the first two weeks of listing are often negotiable. This is where seller credits, price reductions, and flexible terms are most available. Your agent should be filtering for these opportunities actively.

Build your reserve cushion before you close. I recommend that federal buyers in the current environment have at least six months of mortgage payments in accessible savings before closing — not just three months, which is the typical recommendation. This is not pessimism; it's prudence. Six months of reserves means that if something unexpected happens to your employment, you have time to respond strategically rather than reactively.

Frequently Asked Questions from Federal Employees

Q: Are home prices falling in DC because of the federal layoffs?

In DC proper, yes — modestly. Bright MLS projects approximately a 1% price decline for DC in 2026, making it the only Mid-Atlantic market with a projected dip. Active inventory in DC is up over 50% year-over-year. In the Maryland suburbs — Montgomery County and Prince George's County — prices are holding or showing modest appreciation of 1–4%, and the inventory increase is smaller. The impact is real but concentrated in DC proper and some neighborhoods with historically high federal worker concentrations.

Q: Can I still get a mortgage if I'm a federal employee right now?

Yes, absolutely. Federal employment income is treated like any other W-2 employment by mortgage lenders. You'll need to document two years of employment history, provide recent pay stubs and W-2s, and pass standard underwriting. Lenders do verify employment before closing, so if there is any genuine uncertainty about your position, disclose it to your lender early. There are no special restrictions on federal employee mortgages — the challenge is personal employment stability, not lender policy.

Q: What happens to my mortgage if I lose my federal job?

Your mortgage obligation doesn't change if your employment changes — you remain responsible for the payment regardless of employment status. This is why I recommend six months of reserves for federal buyers in the current environment. If you were to lose your job, your options would include using savings to cover payments while seeking new employment (the DC private sector market for government-adjacent skills remains active), renting out a room or the property if needed, requesting forbearance from your lender if facing genuine hardship, or in a worst case, selling — which in a market with modest appreciation still likely means recovering your equity intact. The risk is real but manageable with proper reserves and planning.

Q: Should I use my TSP or federal retirement savings for a down payment?

Generally no, and I'd strongly encourage you to talk with a financial advisor before doing so. TSP withdrawals before age 59½ typically trigger income taxes plus a 10% penalty, which can eliminate the financial advantage of the down payment significantly. TSP loans are a somewhat different calculation — they don't trigger tax penalties, but they reduce your retirement account growth and must be repaid in full if you leave federal service, which creates risk if your employment situation is uncertain. Most federal buyers are better served by using personal savings, exploring Maryland's down payment assistance programs, or accepting a slightly smaller down payment and keeping TSP intact.

Q: Which DC and Maryland neighborhoods have the highest concentration of federal workers?

In DC proper: Capitol Hill, Navy Yard, Southwest Waterfront, Petworth, and Columbia Heights have traditionally had high federal worker populations. In Maryland: Silver Spring, Rockville, Bethesda (NIH corridor), and the areas around Suitland (PGCAR data center area), Greenbelt (NASA Goddard), and Laurel/Beltsville (NSA/Fort Meade commuter shed) all have strong federal worker presence. Notably, some of these neighborhoods are currently seeing the most inventory increase — which, for stable buyers, represents opportunity rather than cause for alarm.

Q: I'm a contractor, not a direct federal employee. Does this guidance apply to me?

In general terms, yes — but your specific risk assessment depends on your contract, your company, and your customer agency. The framework I'd use: if your contract has been renewed recently, your company has diversified revenue (government and commercial), and your customer agency is not under active DOGE scrutiny, you have a reasonably stable employment picture and the buy/wait analysis looks similar to a career federal employee. If your contract renewal is uncertain or your company is heavily concentrated in at-risk agencies, treat your situation more like a probationary employee and rent first. When in doubt, have a frank conversation with your employer about your contract status before committing to a purchase.

The Bottom Line for Federal Buyers

The DC and Maryland housing market in 2026 is not what it was in 2021, and it's not what the more alarming headlines suggest either. For stable federal employees and contractors, it is a market with genuine opportunity — more inventory, more flexible sellers, and a price environment that has moderated from its peak.

The key is honest self-assessment. Know your employment situation clearly before you make a commitment. Build your reserves. Anchor your search to your commute. And work with an agent who will give you a straight read rather than telling you what you want to hear.

If you're a federal employee or contractor trying to work through this decision, I'm here to help — and I'll be as direct with you as I've been in this article.

Are You a Federal Employee or Contractor Looking to Buy in DC or Maryland?

I've helped federal employees and contractors navigate this exact decision — including during periods of genuine uncertainty. I'll give you a straight read on whether buying makes sense for your situation right now, which neighborhoods fit your budget and agency location, and what to expect from the market. No fluff, no pressure.

Call or text Ryan Hehman | 443-990-1230 | Ryan.Hehman@Compass.com

Free consultation. 30 minutes. No obligation.

Related articles on this site:

Relocating to Washington DC & Maryland: The Complete 2026 Guide from a Local Expert

DC vs. Maryland Suburbs: Where Should You Actually Live When Relocating to the DC Area?

Is It Better to Rent First or Buy Immediately When Moving to the DC Area?

How to Buy a Home in DC or Maryland Before You Move: A Step-by-Step Guide

Montgomery County vs. Prince George's County, Maryland: Which Is Right for You?