Down Payment Requirements in Prince George's County, MD (2026): How Much Do You Actually Need and What Assistance Is Available?

Most buyers in Prince George's County need between 3% and 5% down to purchase a home — but if you qualify for the right programs, you could dramatically reduce that number or eliminate it entirely. With a median home price around $430,000–$449,000 in PG County as of early 2026, a standard 3.5% FHA down payment comes to roughly $15,000. That's real money — but here's what a lot of buyers don't know: Prince George's County offers one of the most generous down payment assistance programs in the entire DC metro area, and most buyers never take advantage of it. This guide breaks down exactly what you need, what's available, and how to stack assistance programs to get into your home with as little out of pocket as possible.

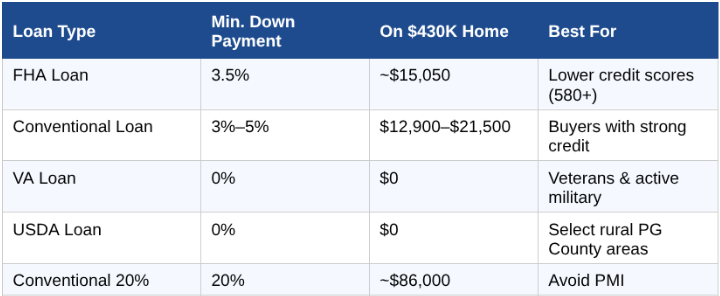

How Much Down Payment Is Actually Required?

Your minimum down payment depends on the type of mortgage loan you use. Here's how the most common loan types break down for a PG County home purchase in 2026:

For most first-time buyers in PG County, an FHA loan with 3.5% down is the most practical starting point — especially if your credit score is in the 580–680 range. Conventional loans at 3%–5% down work well for buyers with stronger credit (typically 680+). Veterans should always explore the VA loan first since no down payment is required and there's no private mortgage insurance.

That said, the down payment is only part of what you'll need at closing. Budget an additional 2%–4% of the purchase price for closing costs — things like title fees, transfer taxes, lender fees, and prepaid items. In PG County, the combined state and local transfer taxes add up, so I always make sure my buyers get a realistic closing cost estimate before they go under contract.

The Programs That Can Change the Math Completely

Here's where PG County separates itself from almost every other jurisdiction in the DC area. Between county-level and state-level assistance programs, eligible first-time buyers can access a stack of funding that covers a substantial portion — or in some cases all — of their down payment and closing costs.

1. Prince George's County Pathway to Purchase

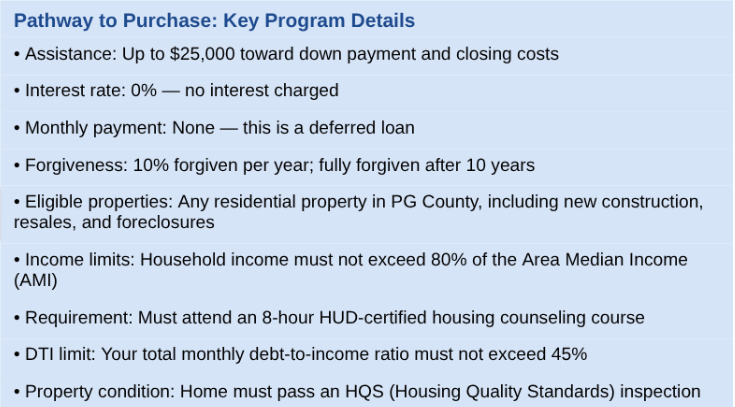

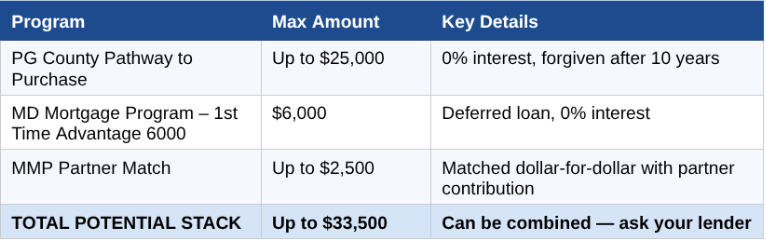

This is the big one. PG County's Pathway to Purchase program provides up to $25,000 in down payment and closing cost assistance for eligible first-time buyers purchasing anywhere in the county. The assistance comes as a 0% interest, deferred payment loan — meaning no monthly payments. The loan amount decreases by 10% per year, and after 10 years it's completely forgiven and the lien is released. If you stay in the home for 10 years, this money is essentially free.

2. Maryland Mortgage Program (MMP) — 1st Time Advantage

The Maryland Mortgage Program offers first-time buyers 30-year fixed-rate mortgages at competitive rates, paired with down payment assistance. The 1st Time Advantage 6000 product provides $6,000 toward your down payment and closing costs as a 0% deferred loan — due only when you sell, refinance, or pay off the mortgage. Other MMP products offer assistance equal to 3%, 4%, or 5% of your loan amount, which on a $430,000 purchase could mean $12,900–$21,500 in additional help.

3. MMP Partner Match

If you pair the MMP 1st Time Advantage 6000 with a qualifying partner contribution (such as from an employer, builder, or community organization), the Maryland Mortgage Program will match that contribution dollar-for-dollar up to $2,500. That brings the 1st Time Advantage 6000 total to as much as $8,500 in assistance.

How the Programs Stack Together

The real power here is that you can combine these programs. Here's what the stack can look like for an eligible PG County buyer in 2026:

To put that in context: on a $430,000 home, a 3.5% FHA down payment is about $15,050. With $33,500 in stacked assistance, your out-of-pocket down payment could be reduced to near zero — with remaining assistance covering a large portion of your closing costs. Not everyone will qualify for the maximum amounts across all programs simultaneously, but even qualifying for the Pathway to Purchase alone can be transformative.

Who Qualifies for These Programs?

The core eligibility requirements for Pathway to Purchase and the Maryland Mortgage Program overlap significantly. Here's the general picture:

You must be a first-time homebuyer (defined as someone who has not owned a primary residence in the past three years — veterans may qualify even if they have owned before)

Your household income must fall within program limits based on the Area Median Income (AMI) for Prince George's County — verify current limits with a participating lender

You must be purchasing in Prince George's County (Pathway to Purchase) or Maryland (MMP)

The property must be your primary residence

You must work with an MMP-approved lender to access these programs

For Pathway to Purchase specifically, the home must pass an HQS inspection and you must complete an 8-hour HUD-certified housing counseling course.

One thing I tell every buyer I work with: talk to a lender before you assume you don't qualify. I've seen buyers who were certain they made too much — and turned out to be well under the limit. The income thresholds are tied to the local AMI, which factors in PG County's cost of living, and they're higher than most people expec

What I'm Seeing on the Ground in PG County

In my work with buyers along the Route 1 corridor — in Hyattsville, Riverdale Park, College Park, and the surrounding communities — I see the same pattern repeatedly: buyers assume they need $20,000–$30,000 saved before they can even start looking. Then they learn about Pathway to Purchase and realize they could be under contract within 60–90 days.

A few realities that matter here. First, funding availability can fluctuate — Pathway to Purchase is subject to available county funds, and there have been periods where the program ran low. If you're thinking about buying, starting the process sooner rather than later is always the right call. Second, the HQS inspection requirement means the home needs to be in reasonable condition — this can occasionally create friction on fixer-upper purchases or distressed properties.

Third, and most importantly: these programs require working with an approved lender and a knowledgeable real estate agent. The process involves coordinating between the county, your lender, and your agent — and the timing matters. I've helped buyers navigate this process many times, and having someone in your corner who's done it before makes a meaningful difference.

Why Route 1 Is the Smart Move for Assistance-Eligible Buyers

PG County's Pathway to Purchase assistance applies anywhere in the county, but I'd argue the Route 1 corridor — Hyattsville, Riverdale Park, College Park, Mount Rainier — offers the best combination of eligibility, value, and long-term upside for buyers using these programs.

Here's why:

Median home prices in Hyattsville (~$419K) and Riverdale Park (~$540K) fall within realistic ranges for assistance-eligible buyers, unlike some pricier parts of the county

Both the Green Line (College Park and Greenbelt Metro stations) and the upcoming Purple Line (expected to open late 2027) provide serious transit infrastructure that supports long-term home values

The Arts District in Hyattsville and Riverdale Park Station's mixed-use development have driven neighborhood investment that rewards buyers who get in now

The area's proximity to University of Maryland, NASA Goddard, and federal facilities in the DC corridor creates a stable, diverse buyer and renter pool

Frequently Asked Questions

Q: Can I buy a home in Prince George's County with no money down?

Potentially, yes — but it requires the right combination of factors. VA loans for veterans and USDA loans for properties in eligible areas offer true zero-down options. For non-veteran buyers, stacking the Pathway to Purchase program with the Maryland Mortgage Program can bring your out-of-pocket down payment very close to zero, though you'll still need some reserves for closing costs not covered by assistance.

Q: How long does it take to get Pathway to Purchase funds?

Budget at least 21 business days from when your full application is submitted to program approval — this is separate from your mortgage approval timeline. Your lender and agent need to coordinate closely to make sure the HQS inspection, mortgage underwriting, and county approval all line up for a smooth closing. Starting the process early is essential.

Q: Does the Pathway to Purchase program affect how much home I can buy?

The program currently has property price limits — verify the current cap with a participating MMP lender, as these figures are subject to change. The program works for resale homes, new construction, short sales, and foreclosures, provided they pass the HQS inspection and meet other program guidelines.

Q: What's the difference between the Pathway to Purchase loan and a grant?

Pathway to Purchase is technically a deferred loan, not a grant — but it functions like a grant if you stay in the home for 10 years, at which point it's completely forgiven. Before 10 years, if you sell or transfer the property, the remaining balance (reduced 10% per year) becomes due. There are no monthly payments and no interest charged at any point.

Q: I make a decent salary — will I still qualify for these programs?

Possibly. Income limits are based on the Area Median Income for Prince George's County, and they're higher than many buyers assume. Household size also matters — a family of four has a higher limit than a single buyer. The only way to know for certain is to speak with an MMP-approved lender who can run the numbers for your specific situation.

Ready to Buy a Home in Prince George's County?

I help buyers navigate PG County's assistance programs and the Route 1 market every day.

Call or text Ryan Hehman at 443-990-1230 to start your home buying journey.

Or email Ryan.hehman@compass.com to schedule a free buyer consultation.

Local expertise. No national hotlines. No pressure.

A note on program details:

Down payment assistance program terms, amounts, and availability change. The figures in this article reflect publicly available information as of April 2026. Always verify current program details and income limits with a participating Maryland Mortgage Program lender before making any decisions. Ryan Hehman is a licensed real estate agent with Compass; he is not a mortgage lender or financial advisor.