10 First-Time Homebuyer Mistakes to Avoid in Maryland

A Hyperlocal Guide for Buyers in the DC Suburbs, Prince George's County & the Route 1 Corridor

The most common first-time home buyer mistakes in Maryland aren't about picking the wrong house, it’s about not knowing the lay of the land . And if you're buying in the DC suburbs, specifically along the Route 1 corridor in Prince George's County, the stakes are even higher. The dual tax structure, flood zone variability, pre-war housing stock, assistance program rules, and a transit picture that's about to shift dramatically with the Purple Line — these are things no national home-buying checklist will tell you. This guide is written specifically for first-time buyers in Hyattsville, Riverdale Park, College Park, Mount Rainier, and the surrounding PG County communities, drawing on what I see go wrong with buyers in this market every single month.

Mistake #1: Skipping Pre-Approval and Starting with the Home Search

I talk to buyers every week who've been browsing Zillow for months before speaking to a lender. In most markets, this wastes time. In the DC suburbs in 2026, it can cost you the house. Homes in Hyattsville and Riverdale Park that are priced well and in good condition routinely go under contract within one to two weeks. If you don't have a pre-approval letter in hand, you can't make an offer sellers take seriously — and in a competitive situation, you simply won't compete.

Pre-approval also clarifies what you can actually afford, which is often different from what online calculators suggest once you factor in PG County's property tax structure, HOA fees, and other carrying costs.

What to do instead:

Get pre-approved before you tour a single home — not during, not after.

Choose a lender familiar with Maryland Mortgage Program and PG County Pathway to Purchase programs, since these require lender coordination that generic national lenders may not handle smoothly.

Keep your pre-approval current — most letters are valid 60–90 days, so don't wait months between approval and offer.

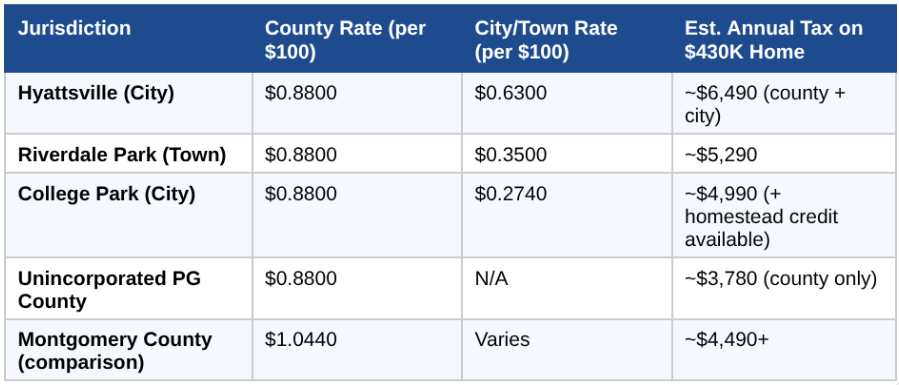

Mistake #2: Not Understanding the Dual Property Tax Structure in PG County

This is the most expensive mistake I see buyers make — and it's 100% preventable. Prince George's County has a layered property tax structure: you pay both a county tax AND a municipal or city tax if the home sits within an incorporated city or town. Most buyers only see the county rate in their mortgage estimate and don't realize there's a second bill coming.

Here's what that actually means for buyers along Route 1 in 2026:

On a $430,000 home, the difference between buying inside Hyattsville city limits versus unincorporated PG County is roughly $2,700 per year — about $225 per month in additional property taxes. That's significant, and it directly affects what you can afford. Some buyers who thought they could comfortably afford a $430K home in Hyattsville are genuinely surprised when their lender runs the full payment with accurate local tax data.

College Park has a partial offset — the city offers a Homestead Property Tax Credit that can meaningfully reduce your tax burden once you've lived in the home for a year, but you must apply for it. It doesn't happen automatically.

What to do instead:

Before you fall in love with a specific address, look up whether it's inside city/town limits or unincorporated county — your agent should be able to tell you instantly.

Ask your lender for a payment estimate using the actual tax rate for that specific address, not a county average.

If you're in College Park, apply for the Homestead Property Tax Credit in your first year of ownership — it caps future assessed value increases.

Mistake #3: Ignoring Flood Risk as an Address-Level Variable

The Route 1 corridor runs along the Anacostia watershed. That means flood risk along this stretch of PG County is not uniform — it varies block by block. One house on a street may be in a standard insurance zone; the next property two doors down may be in a FEMA Special Flood Hazard Area (SFHA) requiring mandatory flood insurance as a condition of your mortgage.

Flood insurance isn't cheap — National Flood Insurance Program (NFIP) policies typically run $800–$2,000+ per year depending on the property's flood zone designation and elevation. That's a carrying cost buyers often discover for the first time at closing, when it's far too late to reconsider the purchase.

There's also an FHA-specific wrinkle worth knowing: properties in certain SFHA designations may not qualify for FHA financing at all. Since many first-time buyers in this market use FHA loans, this is a real deal-killer that can surface late in the process if no one checked the flood map early.

What to do instead:

Before making an offer on any Route 1 corridor home, look up the address at msc.fema.gov to check the FEMA flood zone designation.

If the home is in Zone AE or similar high-risk zone, get a flood insurance quote before you're under contract so you know the real monthly cost.

If you're using FHA financing, confirm with your lender early whether the specific flood zone designation affects loan eligibility.

Mistake #4: Underestimating What Older Housing Stock Actually Costs to Own

The Route 1 corridor is lined with charming pre-war and mid-century homes — Craftsman bungalows, Victorian-style homes, cape cods from the 1940s and '50s. This is part of what makes neighborhoods like Hyattsville Arts District and Riverdale Park so appealing. But these homes come with ownership realities that newer construction doesn't.

Buyers who focus only on purchase price and mortgage payment often miss the maintenance reserve they need for older homes. A 1940s-era house may have an aging roof, galvanized plumbing, an undersized electrical panel, single-pane windows, or a knob-and-tube wiring remnant that insurance companies won't cover. None of these are dealbreakers — but every one of them is a cost you need to plan for.

Maryland's climate also means specific inspection requirements matter here. Radon levels are elevated in parts of PG County. Termite pressure is real in Anacostia-adjacent areas. Sewer laterals in older neighborhoods can be damaged clay pipe, or cast iron which has rusted and closed up over the years. These aren't always red flags but they are budget line items that belong in any honest conversation about buying an older home.

What to do instead:

Budget a maintenance reserve of 1%–2% of the home's value per year on top of your mortgage payment — this is especially important for homes built before 1970.

Don't skip specialty inspections. Beyond the standard home inspection, budget for: radon test (~$150), sewer scope (~$200–300), and a full electrical review on pre-1960 homes.

Ask your agent to review the seller's disclosure carefully for any permitted work history. Unpermitted additions or renovations in older PG County homes are more common than you'd think and can affect financing.

Mistake #5: Not Knowing About — or Properly Applying for — Assistance Programs

Prince George's County has one of the most generous first-time buyer assistance programs in the entire DC metro area. The Pathway to Purchase program offers up to $25,000 in down payment and closing cost assistance as a 0% interest, forgivable loan — and it can be combined with Maryland Mortgage Program assistance for a total stack that can reach $33,500 or more. I wrote a full breakdown of this in a separate post, but the short version is: many buyers who could use this money never access it.

The two most common reasons? They didn't know it existed, or they used a lender who wasn't familiar with how to process it. Pathway to Purchase requires coordination between an MMP-approved lender, a county HQS inspection, and specific application timing. If your lender hasn't done this before, the process falls apart.

What to do instead:

Research PG County Pathway to Purchase and the Maryland Mortgage Program before you choose a lender — not after.

Work with an MMP-approved lender who has specifically processed Pathway to Purchase applications before.

Complete the required 8-hour HUD-certified housing counseling course early in your process — it's a program requirement and it's genuinely useful.

Don't assume you make too much to qualify. Income limits are tied to the local AMI and are higher than most buyers expect.

Mistake#6: Misreading the Market — Assuming Everything Is Competitive (Or Isn't)

The PG County market in 2026 is nuanced. The county-wide median price is around $430,000–$449,000, homes are averaging roughly 50+ days on market, and there has been some price softening year-over-year in parts of the county. Some buyers read this and think they have significant negotiating leverage on everything. That's not quite right.

The truth is that the market is extremely neighborhood-specific. A well-priced, well-maintained home in the Hyattsville Arts District or near Riverdale Park Station can still attract multiple offers. Meanwhile, an overpriced or condition-challenged property in a less-active part of the county may sit for 90+ days with room to negotiate. Treating the whole county as one market leads buyers to either overpay on competitive properties or low-ball on situations that won't work.

What to do instead:

Ask your agent for the specific days-on-market and list-to-sale price ratio for the exact neighborhood and price range you're targeting — not the county average.

If a home has been on the market 45+ days with no price reduction, find out why before assuming it's a negotiating opportunity. Condition and financing issues are often the real answer.

In neighborhoods near confirmed Purple Line stations — Riverdale Park, College Park — factor future transit value into your offer strategy.

Mistake #7: Waiving the Home Inspection to Win an Offer

In the peak seller's market years of 2021–2022, buyers in PG County and across the DC suburbs routinely waived home inspections to compete. Some agents still encourage this in 2026 as a default offer-strengthening strategy. I think it's almost always a mistake, and on Route 1 corridor homes specifically, it's a particularly bad one.

The older housing stock in Hyattsville, Riverdale Park, and Mount Rainier has decades of deferred maintenance, permitted and unpermitted work, and structural idiosyncrasies that a good inspector will catch. I've seen buyers in this market discover $20,000+ in deferred issues after closing that an inspection would have surfaced. The inspection contingency is one of your most important financial protections as a buyer — don't trade it away unless the market genuinely demands it and you have significant cash reserves.

What to do instead:

There are smarter ways to compete: one strategy is a pre-offer inspection, where you do a “walk and talk inspection” before you write the offer. It’s usually a little cheaper than a full inspection with a report, and it focuses on the major systems of the home: plumbing, electrical, HVAC, roof, and structure. I’ve helped many clients in competitive situations get these inspections done so they can submit a clean offer with no inspection contingency, but still have peace of mind with their purchase.

Mistake #8: Not Thinking About the Purple Line When Evaluating Location

The Purple Line light rail — connecting Bethesda to New Carrollton through College Park, Riverdale, and Hyattsville — was approximately 87–90% complete as of early 2026 and is currently targeting a late 2027 opening. This is the most consequential transit development in PG County in decades, and first-time buyers who aren't factoring it into their location decisions are leaving long-term value on the table.

Properties within walking distance of confirmed Purple Line stations — particularly in Riverdale Park, College Park, and the Hyattsville area — have historically outperformed the surrounding market in appreciation as transit projects near completion. This is a well-documented real estate pattern, and the Route 1 corridor is positioned squarely in the zone of maximum impact.

For first-time buyers, this matters in two ways: proximity to a Purple Line station may meaningfully affect the long-term value of the home you're buying, and it affects your commute math if you work in Montgomery County, Bethesda, or the DC core.

What to do instead:

When evaluating homes, check which Purple Line station is nearest and how walkable the route actually is — not just the distance on a map.

Properties within a 10-minute walk of a confirmed station are likely to see stronger appreciation as the opening date approaches.

Don't dismiss Riverdale Park or College Park as "too close to the construction" — that discount often reverses dramatically once a transit line opens.

Mistake #9: Confusing What You're Pre-Approved For With What You Can Comfortably Afford

Lenders will approve you up to the maximum amount your income and debt-to-income ratio technically supports. That number is often higher than what you can actually afford to live comfortably — especially in Maryland, where carrying costs extend well beyond the mortgage payment.

In PG County specifically, your real monthly cost on a $430,000 home might look like this: principal and interest (~$2,700–$2,900 at current rates), property taxes ($300–$540 depending on city/county structure), homeowner's insurance (~$130–$160), PMI if less than 20% down (~$100–$180), flood insurance if applicable (~$70–$170). That's a realistic total monthly payment of $3,300–$4,000+ — which a lender's pre-approval letter based on purchase price alone will not show you.

What to do instead:

Build your own full payment estimate before setting your price ceiling: mortgage + taxes + insurance + HOA (if any) + PMI + flood insurance.

Use the specific property tax rate for the actual neighborhood you're targeting — city of Hyattsville rates are significantly higher than unincorporated county rates on the same purchase price.

Budget a minimum of 1% of the home's value per year as a maintenance reserve — this is a real cost, not optional.

Mistake #10: Working With an Agent Who Doesn't Know This Specific Market

This is the one mistake that makes all the others more likely to happen. The Route 1 corridor is a specific, hyperlocal market with its own dynamics: dual tax structures, Pathway to Purchase coordination, Purple Line-driven pricing differentials, flood zone variables, older housing stock inspection considerations, and neighborhood-by-neighborhood days-on-market patterns. A generalist agent who works across all of Maryland or who primarily covers Montgomery County or Northern Virginia may not know these details at the level that protects you.

What to do instead:

Interview your agent specifically about their experience in the neighborhoods you’re interested in.

Ask how many transactions they've closed in the specific neighborhood you're targeting in the past 12 months.

Frequently Asked Questions

Q: Is it a good time to buy a first home in Prince George's County in 2026?

For buyers who qualify for the Pathway to Purchase and Maryland Mortgage Program assistance, 2026 is an unusually favorable window. The market has softened slightly from its 2022–2023 peak, giving buyers more negotiating room and more inventory to choose from. Interest rates remain elevated but stable. The Purple Line's approaching completion means transit-adjacent neighborhoods on the Route 1 corridor are likely to appreciate meaningfully once the line opens — buyers who get in now capture that upside.

Q: How much do I need saved to buy my first home in Maryland?

With FHA financing and PG County Pathway to Purchase assistance, a qualified first-time buyer could potentially close with as little as $5,000–$10,000 in personal funds, depending on purchase price and how much assistance they qualify for. Without assistance programs, plan on 3.5%–5% for the down payment plus 2%–3% for closing costs. On a $430,000 home, that's roughly $23,000–$34,000 without assistance.

Q: Do I have to use a specific lender to get Pathway to Purchase funds?

Yes — you must work with an MMP-approved lender to access both the Maryland Mortgage Program and PG County's Pathway to Purchase program. The county coordinates directly with your lender, not with you independently. Not all lenders are approved, and not all approved lenders have extensive experience processing Pathway applications. Ask specifically about their Pathway to Purchase track record before committing.

Q: What inspections are most important for homes on the Route 1 corridor?

Standard home inspection, sewer scope (clay pipe laterals are common in pre-1970 homes throughout Hyattsville and Riverdale Park), radon test (PG County has moderate to elevated radon levels in some areas), and a termite/WDO inspection. If the home is near the Anacostia watershed, confirm the flood zone status before the inspection and budget for flood insurance if the property is in Zone AE or similar.

Q: How will the Purple Line affect home values along Route 1?

Transit investments historically drive 10%–25% appreciation premiums within walking distance of new stations in the years surrounding opening. The Purple Line runs directly through the Route 1 corridor — with stations in Riverdale Park and College Park among the most directly impactful for this market. Buyers purchasing in 2026, before the anticipated late-2027 opening, are positioned to benefit from that appreciation window.

Buying Your First Home on the Route 1 Corridor?

I work with first-time buyers in Hyattsville, Riverdale Park, College Park, and throughout Prince George's County every day.

I know the tax structures, the flood zones, the Purple Line impact, and the assistance programs — because I live and work here.

Call or text Ryan Hehman at 443-990-1230

Free buyer consultations. No pressure.

Email: Ryan.Hehman@compass.com