How to Sell Your House Without Losing Money on Repairs

A Seller's Guide to Strategic Repairs, Smart Credits & the Route 1 Corridor Market in 2026

The biggest repair mistake PG County homeowners make before selling is spending money they don't have to spend — and in many cases, not recovering it. Most sellers I work with in Hyattsville, Riverdale Park, and College Park assume they need to fix everything before listing. They don't. The question isn't "what should I repair?" — it's "which repairs will actually affect my price or my ability to sell, and which ones are money I'll never see again?" Those are very different questions, and getting the answer right can be the difference between walking away with $15,000 more or less from your closing.

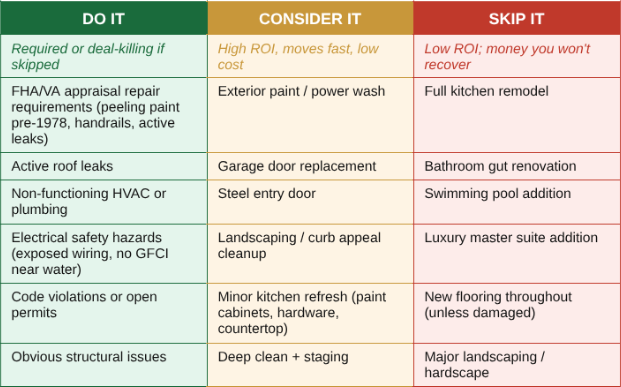

The Core Framework: Three Categories of Repairs

Every repair decision a seller faces falls into one of three buckets. Understanding which bucket a repair belongs in will save you from writing checks you don't need to write.

What Actually Affects Your Sale Price (And What Doesn't)

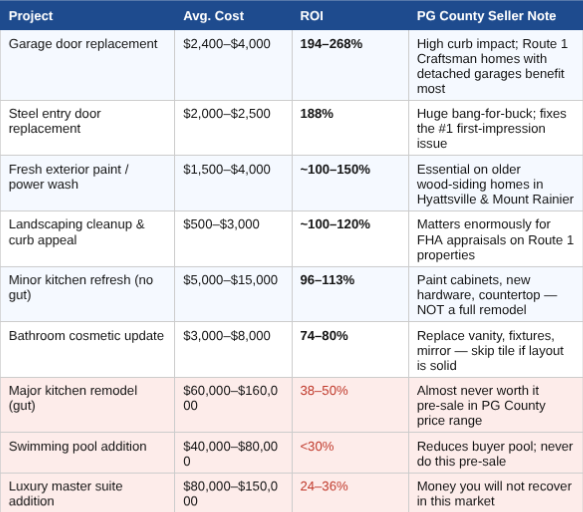

Here's the uncomfortable truth about home repairs before selling: most major renovations return less than 60 cents on every dollar spent. The national data from the Zonda Cost vs. Value Report is consistent on this year after year. A gut kitchen remodel that costs $80,000 might add $38,000 to your sale price in the best case. You've just spent $42,000 you'll never recover. In Prince George's County, where the median home price is around $430,000–$450,000 as of early 2026, this math is even less forgiving — buyers at this price point are looking for clean and functional, not renovated to a spec they didn't choose.

Contrast that with exterior improvements, which the same data shows consistently return more than buyers pay:

Rows highlighted in red = money you'll likely lose. Avoid these pre-sale.

The PG County Wrinkle: FHA Buyers and What They Require

This is where selling in Prince George's County differs from selling in other markets, and it's something every seller on the Route 1 corridor needs to understand. A very large share of buyers in Hyattsville, Riverdale Park, and College Park are using FHA financing — often paired with programs like PG County's Pathway to Purchase assistance. FHA loans come with appraisal requirements that conventional loans don't have. If your buyer is using FHA financing and the appraiser flags certain conditions, those items must be repaired before closing. You don't get to choose.

FHA appraisers flag and require repair of:

Peeling, chipping, or deteriorating paint on any exterior or interior surface of a home built before 1978 (lead paint concern)

Missing handrails on stairs of three or more steps

Active roof leaks or evidence of moisture intrusion

Non-functioning utilities — HVAC, plumbing, electrical panels

Standing water or active drainage problems in crawlspace or basement

Exposed wiring or electrical hazards

Broken windows or inoperable doors

The critical point: seller credits cannot substitute for FHA-required repairs. If the appraiser calls out peeling exterior paint on a 1950s-era Hyattsville bungalow, you must fix the paint — you can't give the buyer $2,000 at closing and call it done. The lender won't close the loan. I've seen deals fall apart at this exact point when sellers didn't anticipate FHA requirements on older homes.

Quick pre-listing check for Route 1 corridor homes:

• Pre-1978 home? Walk every exterior and interior surface for peeling or flaking paint — these are FHA non-negotiables

• Check all stairways for handrails — missing handrails on 3+ steps are flagged by every FHA appraiser

• Test every window and exterior door for functionality

• Look at the roof visually — obvious sagging, missing shingles, or active leaks must be addressed

• Run every faucet, check under sinks, test HVAC in both heat and cool mode

Fixing these before listing isn't optional — it's what keeps a deal alive.

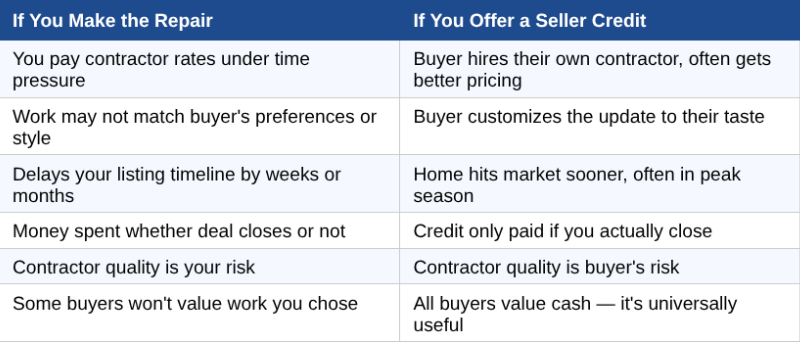

Seller Credits: Often the Smarter Alternative to Making Repairs

Once you've handled FHA-required items and obvious deal-killers, the next question is: should you spend money fixing the rest, or offer the buyer a credit at closing? For most situations I see in PG County, a well-structured seller credit beats a pre-sale repair — financially and logistically.

Here's why seller credits often win:

A practical example: rather than spending $12,000 replacing flooring throughout the house, price the home correctly for its condition and offer a $8,000–$10,000 seller credit. The buyer can use that credit for flooring, closing costs, or an interest rate buydown — whatever serves them best. The home hits the market three weeks sooner, you've spent nothing out of pocket, and the buyer feels like they got a win. That's a deal that closes.

Seller credit limits by loan type (important to know before structuring an offer):

• FHA loans: Seller can contribute up to 6% of the purchase price toward buyer's closing costs

• Conventional loans (under 10% down): Seller can contribute up to 3% of purchase price

• Conventional loans (10–25% down): Up to 6% seller contribution allowed

• VA loans: Up to 4% seller concessions (plus reasonable closing costs)

Always confirm current limits with the buyer's lender before putting a credit amount in the contract.

The Pre-Listing Checklist That Actually Moves the Needle

Based on what I see affect buyer decisions in this specific market — not generic national advice — here's where to put your time and limited budget before listing:

HIGHEST IMPACT: $0–$2,000

1. Deep Clean — Every Surface, Every Room

Professional deep cleaning is the highest ROI pre-listing activity you can do. Buyers — and appraisers — respond to a home that feels cared for. A $300–$600 professional clean changes the energy of every showing. Don't skip this.

2. Declutter and Depersonalize

Buyers need to see themselves in the home. Remove personal photos, excess furniture, and anything that makes rooms feel smaller. Rent a storage unit if needed. Cost: essentially zero.

3. Fix Visible Deferred Maintenance

Running toilets, dripping faucets, stuck drawers, loose doorknobs, patchy caulk — these are cheap to fix and they signal to buyers that the home has been neglected. In PG County, where buyers often have limited reserves, they're hypersensitive to deferred maintenance.

GOOD SPEND: $2,000–$8,000

4. Exterior Curb Appeal

Fresh mulch, trimmed shrubs, a power-washed driveway, seasonal color at the door. For older homes on Route 1 — the Craftsman bungalows, cape cods, and brick colonials — curb appeal is the first impression that sets the entire showing. Budget $500–$3,000 here before anything else.

5. Exterior Paint Touch-Up or Full Paint (if needed)

On pre-1978 homes, this isn't optional if paint is peeling — it's an FHA requirement. But even on newer homes, fresh exterior paint is one of the best ROI improvements you can make. If the exterior looks dated or tired, the buyer's brain starts calculating problems before they've even walked in.

6. Interior Paint — Neutral, Fresh, Top to Bottom

Fresh neutral paint is the single fastest way to make an older home feel updated. In Route 1 corridor homes with original 1950s or 1960s paint colors, this is often the difference between a home that feels move-in ready and one that feels like a project.

7. Entry Door or Garage Door (if yours is dated or damaged)

Per the national Cost vs. Value data, garage door replacement returns 194–268% of its cost, and a new steel entry door returns 188%. If yours looks original to the house and shows its age, this is where $2,000–$4,000 can add $4,000–$8,000 in perceived value. These are the two best purely ROI-driven investments you can make.

CASE-BY-CASE: $8,000+

8. Kitchen and Bathroom: Minor Refresh Only

If your kitchen is functional but dated, a minor refresh — paint the cabinet boxes, new hardware, new countertops, updated faucet — can cost $5,000–$15,000 and return close to what you spent. A full gut renovation at $60,000–$160,000 will not. Same rule applies to bathrooms: new vanity, new mirror, new fixtures, recaulk the tub — yes. Move plumbing, gut tile, full renovation — no.

9. HVAC, Roof, and Major Systems: Disclose Don't Necessarily Replace

If your HVAC is old but functioning, get it serviced and provide records rather than replacing it. A working but aging system is something buyers can negotiate over or plan for. A seller credit or price adjustment is often cleaner than a full HVAC replacement pre-listing. Same principle applies to roofs — if it's past its expected life but not actively leaking, a credit may serve you better than a $15,000–$20,000 replacement. Discuss the specific condition with your agent before committing to either path.

"We Buy Houses" Cash Offers: When They Make Sense (And When They Don't)

Cash buyer companies aggressively target PG County homeowners — you've seen the signs, the mailers, the websites. I want to give you an honest picture of what those offers actually mean, because I've seen sellers lose $40,000–$70,000 by taking cash offers when they didn't need to.

Cash buyers typically offer 60%–75% of market value. On a home worth $430,000, that's a cash offer of roughly $260,000–$322,000. The promise is speed, certainty, and no repairs. For some sellers — those facing foreclosure, probate situations, significant deferred maintenance, or a genuine need to close in 10 days — that trade-off can make sense.

But for most sellers on the Route 1 corridor in reasonable condition, the math doesn't work. You don't need to leave $80,000–$170,000 on the table to avoid repairs. You need a plan that separates what must be fixed (FHA requirements and deal-killers) from what can be offered as a credit (cosmetic and deferred items) from what genuinely doesn't need to be touched.

My recommendation: before accepting any cash offer, call a listing agent and get an honest assessment of what your home would likely sell for on the MLS and what it would cost to get it there. That 30-minute conversation is worth thousands of dollars. I do these walk-throughs at no charge — no obligation to list with me — because I think sellers deserve real information before making a $50,000+ decision.

Frequently Asked Questions

Q: Do I have to make repairs before selling a house in Prince George's County?

Not necessarily — but it depends on how you're selling and who your buyer is. If your buyer is using FHA financing (very common in PG County), an FHA appraiser will flag certain safety and habitability issues that must be repaired before the loan closes — seller credits can't substitute for these. Beyond FHA-required items, most cosmetic or deferred maintenance issues can be handled via price adjustment or seller credit rather than actual repair. An experienced local agent will walk you through what must be fixed versus what can be negotiated.

Q: What repairs have the highest ROI before selling in Maryland?

Exterior improvements consistently outperform interior renovations. A new garage door (194–268% ROI), steel entry door (188%), exterior paint and power wash (~100–150%), and basic landscaping cleanup (~100–120%) are the best pre-sale investments. Inside, a minor kitchen refresh — painting cabinets, new hardware, new countertops without changing the layout — returns close to 100%. Full kitchen or bathroom renovations almost never pay off in the PG County price range.

Q: What's the difference between selling as-is and offering a seller credit?

Selling 'as-is' means you're informing buyers upfront that you won't be making repairs — they buy in current condition. A seller credit means you agree to give the buyer money at closing (typically applied to their closing costs or a rate buydown) in lieu of making a specific repair yourself. Seller credits are often the better strategy because they let the buyer use the money how they want, keep your listing timeline on track, and you only pay if the deal closes. Selling fully as-is typically results in a lower price and a smaller buyer pool.

Q: How much can I offer as a seller credit in PG County?

The maximum seller credit depends on the buyer's loan type. FHA buyers can receive up to 6% of the purchase price. Conventional buyers putting less than 10% down are limited to 3% seller contributions. Conventional buyers with 10–25% down can receive up to 6%. Always confirm the limit with the buyer's lender before structuring a contract — exceeding the limit creates appraisal and underwriting complications.

Q: Should I replace my HVAC or roof before selling?

Usually not — unless they're actively failing and an FHA appraiser would flag them. A working but aging HVAC system or a roof with some years left is something you can disclose, price for, or offer a credit against. Replacing a functioning system pre-sale rarely recovers the cost at closing. Get both serviced, provide maintenance records, and let your agent advise on whether the condition warrants a price adjustment or credit versus a full replacement. In most cases I see, disclosure and credit is the right answer.

Thinking About Selling in Prince George's County?

Before you spend a dollar on repairs, call me. I'll walk through your home, tell you exactly what matters to buyers in this market, what will and won't affect your price, and whether a seller credit makes more sense than a contractor.

You'll get an honest assessment — not a renovation pitch.

Call or text Ryan Hehman at 443-990-12

ryanhehmanrealestate.com | Compass Real Estate | Serving the Route 1 Corridor & PG County