Appraised Value vs. Market Value: What Maryland Home Sellers Need to Know Before Pricing Their Home in 2026

The Short Answer:

Appraised value is what a licensed appraiser says your home is worth based on past sales data. Market value is what a real buyer will actually pay for it today. In a competitive Maryland suburb, those two numbers can easily be $30,000 to $50,000 apart — and which direction that gap falls can make or break your sale. Here's what every homeowner in Prince George's County and Montgomery County needs to understand before pricing their home.

Two Numbers, Two Very Different Jobs

When you start thinking about selling your home, you'll quickly hear two terms that sound similar but mean very different things: appraised value and market value. Confusing them is one of the most common — and costly — mistakes Maryland sellers make.

Let's break them down clearly.

What Is Appraised Value?

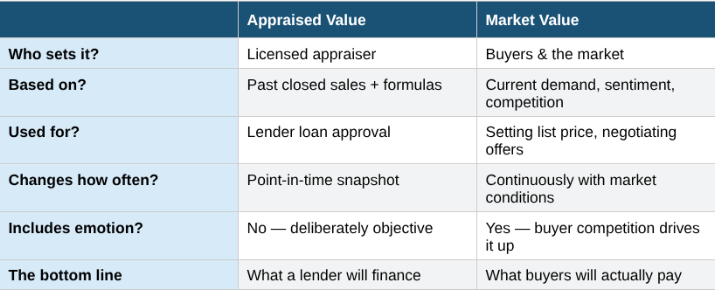

Appraised value is a formal, licensed opinion of what your home is worth based on recent closed sales of comparable homes nearby. A licensed appraiser physically inspects your property, measures square footage, documents condition and features, and applies standardized methods governed by the Uniform Standards of Professional Appraisal Practice (USPAP).

The appraiser's job is to be objective. They don't factor in how much you love the house, how many people toured it last weekend, or how aggressively buyers are competing right now. They look backward — at what similar homes have already sold for — and apply that data to your property.

Appraised value matters most to one party: the lender. When a buyer finances a home, the bank will only loan up to the appraised value. That ceiling is what makes appraisals so important — and why a gap between the appraised value and the sale price can derail a deal.

What Is Market Value?

Market value is something entirely different. It's not determined by a single professional — it's determined by the market itself. Specifically, it's the price a ready, willing, and able buyer will actually pay for your home in today's conditions.

Market value accounts for everything the appraiser deliberately ignores: buyer emotion, competition, timing, interest rates, local inventory, and simple supply and demand. In a neighborhood like Riverdale Park or College Park along the Route 1 corridor, where inventory is historically tight and demand runs high, market value can run well above what an appraiser would put on paper.

Think of it this way: if three buyers compete for your home and the winning offer comes in $25,000 above asking, that final sale price is your market value. An appraiser, working from older closed sales, might not validate that price on paper — which is exactly where things can get complicated.

The Real Problem: When Sellers Use an Appraisal to Set Their Asking Price

Here's where I see Maryland sellers get into trouble — sometimes expensive trouble.

Some sellers, especially those who want an "objective" number before listing, will hire an appraiser to assess their home before it hits the market. The thinking makes sense: get a professional valuation, use it to set your price, and avoid guesswork. On the surface, that sounds prudent. But in practice, it often backfires.

Why Pre-Listing Appraisals Can Work Against You

Appraisals look backward, not forward. An appraiser's job is to look at what similar homes have already sold for — typically in the past 6 to 12 months. In a market where prices are rising, those past sales can actually understate where today's buyers are willing to go. You could end up with an "appraised value" that's conservative compared to what the current market would actually support.

Pre-listing appraisals expire fast. Once you have an appraisal in hand, it starts aging immediately. Real estate markets in Prince George's and Montgomery Counties can shift meaningfully in 90 days. By the time you prep your home, list it, negotiate, and reach the closing table, that appraisal number may no longer reflect current conditions — yet you may have anchored your price to it.

It's not what the buyer's lender will use anyway. Even if you paid for a pre-listing appraisal, the buyer's lender will order their own, independent appraisal. Your appraisal doesn't travel to the closing table with you — it sits in your files.

Overpricing from an inflated appraisal is a seller's worst nightmare. If an appraisal comes in higher than what buyers will actually pay (which can happen in slower market segments or with unique properties), and you price to that number, you'll sit on the market. The longer a listing lingers, the more buyer leverage grows. Homes that sit past the 21-30 day mark in our market begin carrying a stigma — buyers start asking what's wrong with the property, and offers, when they do come, tend to come in lower.

Real Talk from the Field:

I've had seller clients come to me already armed with an appraisal they'd paid $400–$500 for. In some cases, that appraisal was below where I would have recommended listing — meaning they'd already started thinking smaller than the market would support. In others, the appraisal gave them a false sense of confidence that cost them weeks on market.

In both scenarios, the appraisal didn't help them. A current, local Comparative Market Analysis would have been more accurate, more relevant, and completely free.

The Right Tool for Pricing a Maryland Home: The Comparative Market Analysis

The tool that actually helps sellers price correctly is a Comparative Market Analysis — a CMA. Unlike an appraisal, a CMA is prepared by a real estate agent using current market data: active listings competing with yours, homes that recently went under contract, homes that recently closed, and homes that expired without selling (a critically important data point most online tools skip).

A well-prepared CMA from an agent who works your specific market will be more accurate than a pre-listing appraisal for one key reason: it reflects what buyers are doing right now, not what they did six months ago.

In Prince George's County and along the Route 1 corridor — Hyattsville, Riverdale Park, College Park, Mount Rainier — I track buyer activity weekly. I know which price points are generating multiple offers, which neighborhoods are seeing homes go above asking, and where buyer resistance is building. That intelligence doesn't show up in an appraiser's backward-looking report.

Maryland Note:

Under the Maryland Real Estate Commission (MREC) Code of Ethics, a proper Market Analysis can only be completed by a licensed real estate agent, and must include the disclosure: "THIS ANALYSIS IS NOT AN APPRAISAL. IT IS INTENDED ONLY FOR THE PURPOSE OF ASSISTING BUYERS OR SELLERS IN DECIDING THE LISTING, OFFERING, OR SALE PRICE OF REAL PROPERTY." This isn't a limitation — it's an honest acknowledgment that pricing strategy and appraisal methodology are two different disciplines, serving two different purposes.

When a Pre-Listing Appraisal Actually Makes Sense

To be fair, there are situations where getting an appraisal before listing is the right move. These include:

Estate sales — When multiple heirs need an independent, professional opinion of value to make decisions or satisfy legal requirements.

Unique or complex properties — If your home is a true one-of-a-kind with few true comparables (unusual acreage, historic designation, commercial-residential mix), an appraiser's cost and income approach methods may provide useful structure.

Disputes between co-owners — Divorces, partnership dissolutions, or situations where multiple owners disagree on value can benefit from a neutral, licensed third-party opinion.

Out-of-area sellers — If you've inherited a property in Prince George's County but live elsewhere and don't have an established agent relationship, an appraisal can provide an initial reality check.

For most traditional sellers who are simply preparing to list their primary residence? The appraisal isn't necessary — and the money is better spent elsewhere.

What Happens When the Buyer's Appraisal Comes in Low?

Even if you price correctly with a solid CMA, appraisal issues can still emerge — but now on the buyer's side, once you're under contract. This is when understanding the difference between appraised value and market value really matters operationally.

Here's the scenario: You list your Hyattsville home at $450,000. Multiple buyers compete, and you accept an offer at $475,000. The buyer's lender orders an appraisal, and it comes in at $455,000. That $20,000 gap is called an appraisal gap, and now everyone has decisions to make.

Your options as the seller:

Reduce the price to match the appraised value ($455,000)

Negotiate a split — seller comes down some, buyer covers some of the gap in cash

Hold firm and let the buyer cover the full gap out of pocket (only works if the buyer is willing and financially able)

If the buyer walks, relist — though you'll now want to document this for the next buyer's appraiser

In competitive segments of the Route 1 corridor, I've seen buyers proactively waive appraisal contingencies or sign appraisal gap guarantees to win competitive situations. That's a real-time market dynamic no appraisal can predict.

Frequently Asked Questions

Is appraised value the same as market value in Maryland?

No. Appraised value is a point-in-time estimate from a licensed professional based on past comparable sales. Market value is what buyers will actually pay today, shaped by current inventory, demand, and competition. In an active market like Prince George's County, market value frequently exceeds appraised value.

Should I get an appraisal before listing my home in Maryland?

For most sellers, no. A free Comparative Market Analysis from an experienced local agent gives you more actionable, current data at no cost. Pre-listing appraisals can anchor you to a number that doesn't reflect what today's buyers will actually pay, and they don't carry over to the buyer's lender anyway.

What does Maryland's tax assessed value have to do with my listing price?

Very little. Maryland's tax assessed value is calculated by the Department of Assessments and Taxation on a triennial reassessment cycle and is designed to determine your property tax obligation — not your home's sale price. Many Maryland homeowners are assessed well below current market value due to the phase-in system and homestead credit caps. Don't use your assessment to set your asking price.

What happens if an appraisal comes in low after we're under contract?

You have several options: negotiate a price reduction, ask the buyer to cover the appraisal gap in cash, challenge the appraisal with stronger comparable sales data, or relist the property. An experienced agent will help you evaluate which path makes the most financial sense given current market conditions.

How accurate are online home valuations like Zillow Zestimate in Maryland?

Online automated valuation models have improved, but they still have significant error rates — especially in areas with limited transaction volume or unique property characteristics. In off-market properties, Zillow's error rate runs higher. For pricing purposes, rely on a licensed agent's CMA, not an algorithm.

Can a seller's pre-listing appraisal be shared with the buyer?

Yes, but you're generally not required to. However, if the appraisal reveals a material defect or condition issue, Maryland's seller disclosure laws may require you to disclose that underlying information even if you don't hand over the full report. Discuss this with your agent and attorney.

Thinking About Selling in Prince George's or Montgomery County?

Before you spend money on an appraisal or guess at a price, let me run a free Comparative Market Analysis for your home. You'll get real data, real comps, and a real pricing strategy — not a number that might anchor you in the wrong direction.

Ryan Hehman | Home Keys Team of Compass

Call or Text: 443-990-1230

Email: Ryan.Hehman@Compass.com